If you’re a veteran and looking to buy a home, VA loans are an excellent option for you. These loans come with a wide range of benefits that are specifically designed to help veterans navigate the home buying process. From low or even zero down payments to competitive interest rates, VA loans offer a host of advantages that make homeownership more accessible and affordable. Whether you’re a first-time homebuyer or looking to refinance, VA loans provide a valuable opportunity for veterans to achieve their homeownership dreams.

This image is property of www.veteransunited.com.

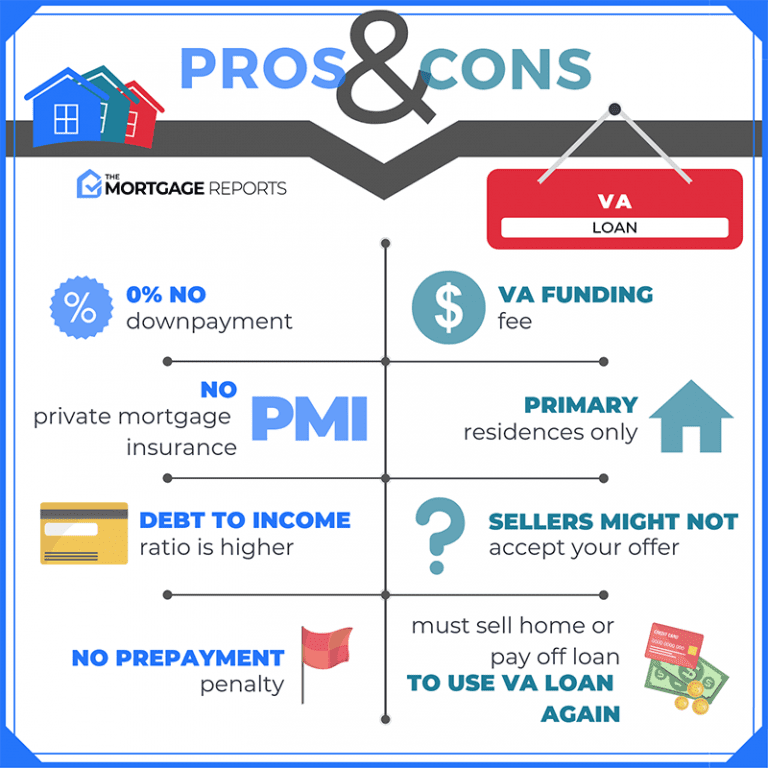

1. No down payment required

1.1 Eligibility for zero down payment

One of the major advantages of VA loans for veterans is that they do not require a down payment. This means that you can finance 100% of the purchase price of your home. Unlike conventional loans which often require a down payment of 20% or more, VA loans allow you to become a homeowner without having to save up for a down payment. This can be a significant relief, especially for veterans who may be starting over after their military service or who may not have the financial means to save for a down payment.

1.2 Eliminating the need to save for a down payment

Saving for a down payment can be a daunting task, particularly for veterans who may be transitioning to civilian life or facing other financial obligations. With VA loans, you can eliminate the need to save for a down payment, allowing you to allocate your savings towards other important expenses or investments. Whether you’re purchasing your first home or looking to upgrade, the ability to finance the entire purchase price can make homeownership more accessible and attainable for veterans.

2. Lower interest rates

2.1 VA loans typically offer lower interest rates

Another significant benefit of VA loans for veterans is the potential for lower interest rates. VA loans are backed by the Department of Veterans Affairs, which provides a guarantee to lenders in case of borrower default. This guarantee reduces the risk for lenders, allowing them to offer lower interest rates to veterans. Lower interest rates can result in substantial savings over the life of the loan, making homeownership more affordable for veterans.

2.2 Reduced monthly payments

In addition to lower interest rates, VA loans can also lead to reduced monthly mortgage payments. With a lower interest rate, your monthly payment amount decreases, allowing you to allocate your hard-earned money towards other essential expenses or savings goals. This can have a significant impact on your overall financial well-being and provide you with greater flexibility in managing your monthly budget, especially for veterans on a fixed income or with other financial obligations.

3. Easier qualification requirements

3.1 Less stringent credit score requirements

Unlike traditional loans that often have strict credit score requirements, VA loans are more forgiving when it comes to credit scores. While lenders still consider your credit history and score, they tend to be more lenient with VA loan applicants. This means that even if you have had some financial challenges in the past, you still have a good chance of qualifying for a VA loan. This flexibility can be incredibly helpful for veterans who may be rebuilding their credit or have limited credit history due to their time in the military.

3.2 Flexible debt-to-income ratio

VA loans also offer more lenient debt-to-income ratio requirements. This means that even if you have existing debts, such as student loans or car payments, you may still be able to qualify for a VA loan. Lenders take into account your ability to repay the loan based on your monthly income and existing debts, allowing for more flexibility and a higher chance of approval. This can be especially beneficial for veterans who may have multiple financial obligations or are still in the process of transitioning into civilian life.

4. No private mortgage insurance (PMI) required

4.1 Saving money by not paying for PMI

Unlike conventional loans, VA loans do not require private mortgage insurance (PMI). PMI is typically required for borrowers who make a down payment of less than 20% in order to protect the lender in case of default. By eliminating the need for PMI, veterans can save a significant amount of money over the life of their loan. This can result in lower monthly mortgage payments and overall housing expenses, providing veterans with more financial flexibility and stability.

4.2 Lowering overall monthly housing expenses

In addition to the savings from not paying for PMI, VA loans can also lower overall monthly housing expenses. With lower interest rates and no down payment requirement, veterans can potentially secure a more affordable monthly mortgage payment compared to traditional loans. This can free up funds for other essential expenses or savings, allowing veterans to better manage their finances and improve their overall financial well-being.

This image is property of www.mbamortgageteam.com.

5. Limits on closing costs

5.1 VA loans restrict the types of closing costs veterans can be charged

VA loans place limits on the types of closing costs that can be charged to veterans. This protects veterans from excessive or unnecessary fees associated with the home-buying process. While there are still some closing costs that veterans are responsible for, such as appraisal fees and title insurance, the overall amount is often significantly lower compared to conventional loans. This reduction in closing costs can help veterans save money upfront, making homeownership more accessible and affordable.

5.2 Saving money on upfront expenses

By limiting the closing costs veterans are responsible for, VA loans allow veterans to save money on upfront expenses. For many individuals, coming up with the necessary funds for closing costs can be a significant barrier to homeownership. By reducing these expenses, VA loans make it easier for veterans to transition into homeownership without breaking the bank. This can provide veterans with a valuable opportunity to build equity and establish a stable foundation for their future.

6. Ability to finance funding fee

6.1 Option to roll the funding fee into the loan amount

VA loans require a funding fee, which helps offset the cost of the loan program for taxpayers. However, one of the benefits of VA loans is the option to roll the funding fee into the loan amount. This means that veterans do not have to pay the funding fee upfront in cash but can instead finance it as part of their overall loan. This can be particularly advantageous for veterans who may not have the immediate funds to cover the funding fee, allowing them to preserve their savings for other purposes.

6.2 Avoiding the need for upfront cash payment

By financing the funding fee, VA loans eliminate the need for an upfront cash payment. This can be a significant relief for veterans, especially those who are just starting their civilian careers or who may be facing financial challenges. By avoiding a large upfront cash payment, veterans can better manage their finances and allocate their resources towards other essential expenses or savings goals. This flexibility can make the home-buying process more manageable and less stressful for veterans.

This image is property of assets.themortgagereports.com.

7. Assumable loans

7.1 Transferring the loan to another eligible veteran

One unique feature of VA loans is the ability to transfer or “assume” the loan to another eligible veteran. Assumable loans can be an attractive benefit for veterans who may need to relocate or sell their home. Instead of going through the process of obtaining a new loan, the buyer can take over the existing VA loan, assuming the same terms and conditions. This can save both parties time and money, as it eliminates the need for new appraisals and loan origination fees. Additionally, assuming a VA loan can potentially save the buyer money on closing costs.

7.2 Potential savings on closing costs for the buyer

Assumable loans not only benefit the seller but also the buyer. By assuming a VA loan, the buyer can potentially save money on closing costs. Since the loan is already in place, there is no need for new loan origination fees or appraisals. This can result in substantial savings for the buyer, allowing them to allocate their funds towards other expenses associated with homeownership. Assumable loans provide a unique opportunity for both sellers and buyers in the real estate market and can be a valuable advantage for veterans.

8. Flexible refinancing options

8.1 Streamline Refinance program for lowering interest rates and monthly payments

VA loans offer flexible refinancing options, which can help veterans reduce their interest rates and monthly mortgage payments. The Streamline Refinance program, also known as the Interest Rate Reduction Refinance Loan (IRRRL), allows veterans to refinance their existing VA loan with minimal documentation and paperwork. This streamlined process helps veterans take advantage of lower interest rates, potentially saving them money over the life of the loan. By refinancing, veterans can also adjust the terms of their loan, such as switching from an adjustable-rate mortgage to a fixed-rate mortgage, providing additional stability and peace of mind.

8.2 Cash-out Refinance program for accessing home equity

In addition to the Streamline Refinance program, VA loans also offer the Cash-out Refinance program. This program allows veterans to access the equity in their homes by refinancing for a higher loan amount than what is currently owed. The difference between the new loan amount and the existing loan amount is provided to the veteran in cash, which can be used for various purposes, such as debt consolidation, home improvements, or other financial needs. The Cash-out Refinance program provides veterans with a valuable financial tool to leverage their home equity and meet their individual financial goals.

This image is property of www.jvmlending.com.

9. Foreclosure avoidance assistance

9.1 VA loan servicers offer foreclosure prevention options

For veterans who may be facing financial difficulties and are at risk of foreclosure, VA loan servicers provide assistance through foreclosure prevention options. The Department of Veterans Affairs works with loan servicers to ensure that veterans have access to resources and support in times of financial hardship. These options may include loan modifications, repayment plans, or other alternatives to foreclosure. The goal is to help veterans stay in their homes and avoid the devastating consequences of foreclosure. This assistance provides valuable peace of mind and financial relief for veterans facing uncertain times.

9.2 Substantial financial relief for veterans facing foreclosure

By offering foreclosure prevention options, VA loans provide substantial financial relief for veterans who may be facing foreclosure. Losing a home is an emotionally and financially distressing situation, and the Department of Veterans Affairs recognizes the importance of helping veterans navigate these challenging circumstances. With access to foreclosure prevention options, veterans have an opportunity to work with their loan servicers to find a viable solution that suits their financial situation. This support not only helps veterans keep their homes but also provides them with a sense of stability and security during difficult times.

10. VA appraisal process

10.1 Ensuring fair value for the property

VA loans have a unique appraisal process that is designed to ensure fair value for the property. This appraisal process helps protect veterans from overpaying for a home and provides assurance that the property meets safety and habitability standards. The appraiser evaluates the property’s market value and compares it to similar properties in the area. This ensures that veterans are getting a fair deal and are not being taken advantage of in the home-buying process. The VA appraisal process provides veterans with additional peace of mind and protection throughout their homebuying journey.

10.2 Protecting veterans from overpaying

The VA appraisal process plays a crucial role in protecting veterans from overpaying for a property. By conducting a thorough evaluation of the property’s value, the appraiser ensures that the purchase price aligns with the fair market value. This can prevent veterans from getting into a situation where they owe more on their mortgage than the property is worth. By protecting veterans from overpaying, the VA appraisal process helps safeguard their financial well-being and ensures that they are making a sound investment for the future.

Unlock This Hidden Part Of Your Credit Report To Access Up To One Million Dollars Without Any Proof Of Incomehttps://lendingsum.com/85l7

This image is property of www.mortgagecalculator.org.