Looking for ways to finance your expenses? Look no further than credit card financing and loan options. Whether you’re looking to make a big purchase or consolidate your debt, understanding the ins and outs of credit card financing and loans can help you make informed financial decisions. From refinancing and interest rates to home equity and credit scores, this article will explore the various aspects of credit card financing and loans. So sit back, relax, and let’s dive into the world of credit card financing and loan options together.

How To Access Up To One Million Dollars Without Any Proof Of Income

Credit Card Financing

Credit card financing is a convenient way to make purchases and manage your expenses. When you use a credit card, you’re essentially borrowing money from the credit card company to pay for your purchases. However, it’s important to understand the terms and conditions of credit card financing to ensure that you’re making informed financial decisions.

Interest Rates

One of the key factors to consider when using credit card financing is the interest rate. The interest rate determines how much it will cost you to borrow money and is expressed as an annual percentage rate (APR). The higher the APR, the more you’ll pay in interest on your outstanding balance. It’s essential to compare interest rates between credit cards to find the one that offers the most favorable terms for you.

Finance Charges

Finance charges are the fees associated with credit card financing. These charges can include things like annual fees, late payment fees, and balance transfer fees. It’s important to review the fee structure of each credit card to understand the total cost of borrowing. Some credit cards may offer lower interest rates but higher fees, so it’s important to consider both aspects when choosing a credit card.

Credit Card Debt

Accumulating credit card debt can be a significant burden on your finances. It’s important to use credit card financing responsibly and only spend what you can afford to pay back. Credit card debt can quickly accumulate if you’re not making regular payments, and the high interest rates can make it difficult to pay off the balance. It’s crucial to have a plan in place to manage and pay off your credit card debt to avoid financial hardship.

Monthly Payments

Credit card financing requires you to make monthly payments on your outstanding balance. These payments typically include both the interest and a portion of the principal amount borrowed. It’s important to make these payments on time to avoid late fees and potential damage to your credit score. By paying more than the minimum monthly payment, you can reduce the overall cost of borrowing and pay off your debt faster.

Grace Period

Credit cards often offer a grace period, which is a window of time during which you can pay your balance in full without incurring any interest charges. This grace period usually lasts between 21 and 25 days from the statement date. To take advantage of the grace period, it’s important to pay your balance in full by the due date. If you carry a balance, the grace period may not apply, and interest charges will start accruing immediately.

Late Payment

Making late payments on your credit card can have significant consequences. Not only will you typically incur late payment fees, but your credit score may also be negatively affected. Late payments can stay on your credit report for up to seven years, making it more difficult to qualify for favorable interest rates on future loans and credit cards. It’s essential to make your credit card payments on time to maintain a good credit history.

Default

Defaulting on your credit card means that you have failed to make the required payments on your outstanding balance. Defaulting can have severe consequences, including additional fees, increased interest rates, and even legal action by the credit card company. Defaulting on your credit card can severely damage your credit score and make it challenging to obtain credit in the future. It’s important to contact your credit card company if you’re struggling to make payments to explore alternative options.

Predatory Lending

Predatory lending refers to unethical lending practices that take advantage of borrowers who may not fully understand the terms and conditions of their loans. Predatory lenders often target individuals with poor credit histories or low-income individuals who are desperate for credit. It’s important to be aware of the signs of predatory lending and to thoroughly review any loan agreements before signing. If you suspect that you’re a victim of predatory lending, it’s crucial to report it to the relevant authorities.

Credit Counseling

Credit counseling is a service provided by nonprofit organizations that can help you manage your credit card debt and improve your financial situation. Credit counselors can offer guidance on budgeting, debt consolidation, and negotiating with creditors. They can also help you understand your credit report and take steps to improve your credit score. Credit counseling can be a valuable resource for individuals struggling with credit card debt and can help you regain control of your finances.

Loan Origination

Loan origination refers to the process of applying for and obtaining a loan. The loan origination process typically includes submitting an application, providing supporting documentation, and undergoing a thorough review by the lender. During the loan origination process, the lender will assess your creditworthiness and determine the terms and conditions of the loan. It’s important to gather all the necessary documents and be prepared for the lender’s scrutiny during the loan origination process.

How To Access Up To One Million Dollars Without Any Proof Of Income

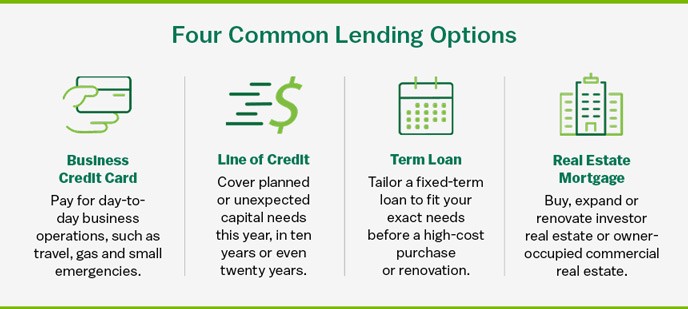

Loan Options

When it comes to obtaining a loan, you have several options to consider. Each type of loan has its own features and requirements, so it’s important to choose the one that best suits your financial needs.

Refinance

Refinancing a loan involves replacing an existing loan with a new loan that has better terms and conditions. Refinancing can help you lower your interest rate, reduce your monthly payments, or change the duration of the loan. Common types of loans that can be refinanced include mortgages and auto loans. Before refinancing, it’s essential to carefully consider the costs associated with refinancing to ensure that it’s a financially advantageous decision.

Personal Loan

A personal loan is a type of loan that is not secured by collateral. Personal loans can be used for a variety of purposes, such as debt consolidation, home improvements, or unexpected expenses. Personal loans typically have higher interest rates than secured loans but offer greater flexibility in how the funds can be used. Before taking out a personal loan, it’s important to carefully review the terms and conditions and assess your ability to repay the loan.

Home Equity Loan

A home equity loan is a type of loan that uses the equity in your home as collateral. Equity is the difference between the current value of your home and the amount you owe on your mortgage. Home equity loans are typically used for large expenses, such as home renovations or debt consolidation. They often have lower interest rates than personal loans and credit cards but carry the risk of foreclosure if you default on the loan.

Mortgage

A mortgage is a loan that is used to purchase a home or other real estate property. The property itself serves as collateral for the loan. Mortgages can have fixed or adjustable interest rates and are usually repaid over a long period, often 15 or 30 years. When applying for a mortgage, lenders will assess your creditworthiness, your income, and the value of the property. It’s essential to carefully consider your financial situation before taking on a mortgage and to shop around for the best terms.

Secured Loan

A secured loan is a loan that requires collateral, such as a car, real estate, or other valuable assets. By providing collateral, you reduce the risk for the lender, which can result in lower interest rates. However, if you default on the loan, the lender has the right to seize and sell the collateral to recover the outstanding balance. Secured loans are often used for large purchases, such as a car or home, and typically have longer repayment terms.

Unsecured Loan

An unsecured loan is a loan that is not backed by collateral. Instead, the lender relies solely on your creditworthiness and income to determine whether to approve the loan. Unsecured loans are typically smaller in size and have higher interest rates than secured loans. They can be used for a variety of purposes, such as debt consolidation, home improvements, or medical expenses. It’s important to carefully review the terms and conditions of an unsecured loan and consider the impact on your overall financial situation.

Consolidation

Debt consolidation involves combining multiple debts into a single loan with a lower interest rate or more favorable terms. This can help simplify your finances and make it easier to manage your debt. Debt consolidation loans can be secured or unsecured, depending on your financial circumstances. It’s important to carefully review your current debts and assess whether debt consolidation is the right option for you.

Bad Credit

Having bad credit can make it difficult to obtain loans and credit cards. Bad credit is typically the result of late payments, high levels of debt, or defaults on previous loans. However, there are options available for individuals with bad credit, such as secured loans or loans from specialized lenders. It’s important to carefully review the terms and conditions of these loans and consider the impact on your overall financial situation.

Loan Term

The loan term refers to the length of time over which the loan will be repaid. Loan terms can vary widely depending on the type of loan and the lender’s requirements. Shorter loan terms often result in higher monthly payments but lower overall interest charges. Longer loan terms can result in lower monthly payments but higher overall interest charges. It’s important to carefully consider your financial situation and goals when choosing a loan term.

Balloon Payment

A balloon payment is a large payment that is due at the end of a loan term. Balloon payments are commonly associated with loans that have lower monthly payments but a large final payment. Balloon payments can be risky if you’re unable to make the payment when it becomes due. It’s important to carefully consider your ability to make the balloon payment and to have a plan in place to cover the cost.

In conclusion, credit card financing and loan options provide individuals with various ways to manage their financial needs. It’s important to carefully consider the terms and conditions of credit cards and loans to ensure that you’re making informed decisions. By understanding interest rates, finance charges, monthly payments, and other key aspects of credit card financing and loan options, you can make sound financial choices and achieve your financial goals. Remember to review your options, compare lenders, and seek professional advice when necessary to make the best possible decisions for your financial well-being.

How To Access Up To One Million Dollars Without Any Proof Of Income