In the world of mortgages, there are two primary options to consider: fixed-rate and adjustable-rate. As a homeowner or potential homebuyer, it is crucial to understand the differences between these two types of mortgages to make an informed decision. Fixed-rate mortgages offer stability and peace of mind with a consistent interest rate throughout the loan term, while adjustable-rate mortgages provide flexibility and the potential for lower initial payments. In this article, we will explore the pros and cons of both options to help you determine which one is the right choice for you.

This image is property of www.investopedia.com.

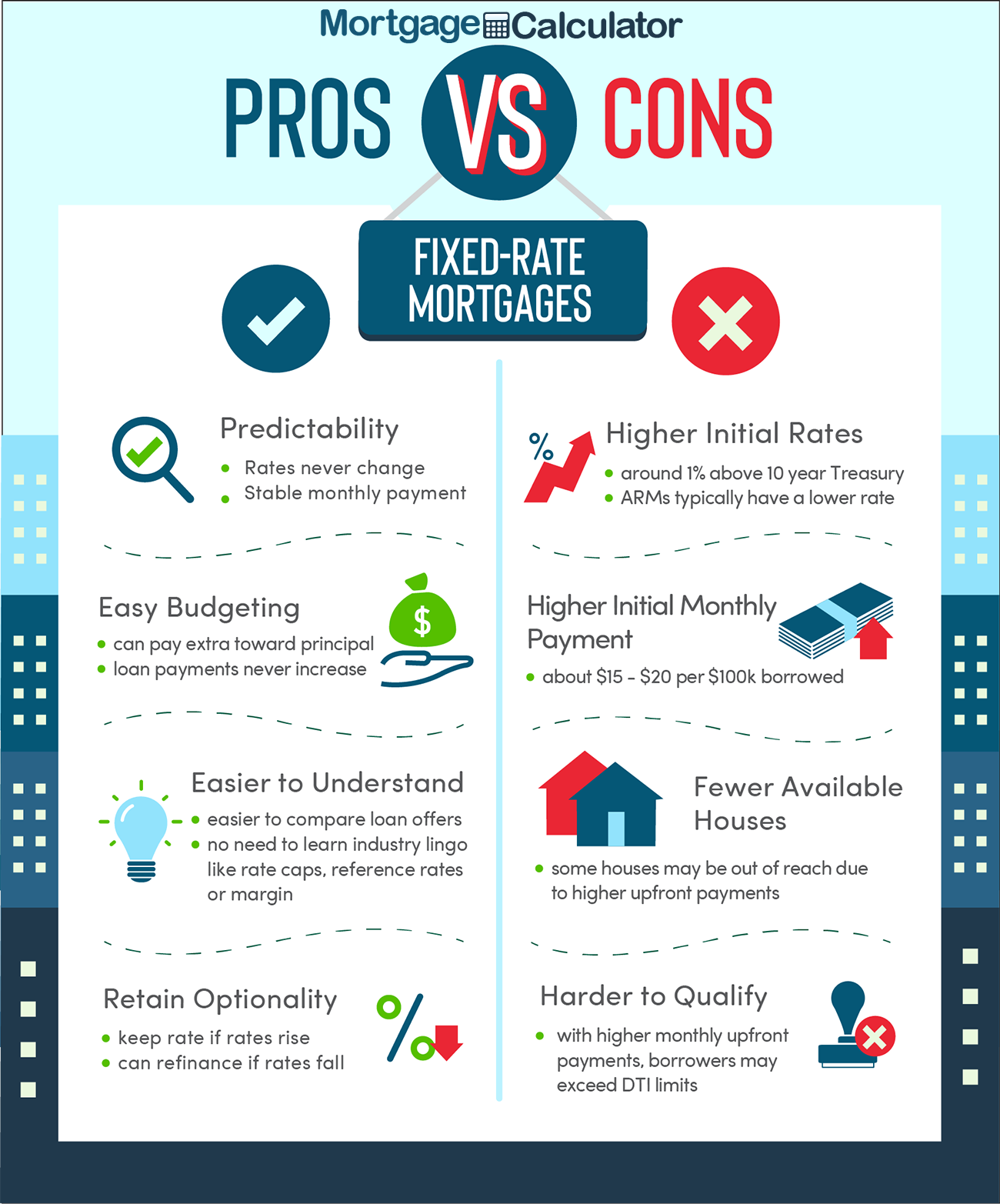

Fixed-rate Mortgages

Definition and Features of Fixed-rate Mortgages

A fixed-rate mortgage is a type of home loan with an interest rate that remains constant for the entire duration of the loan. This means that your monthly mortgage payments will also remain the same throughout the life of the loan, providing you with stability and predictability. The fixed interest rate is typically higher than the initial rate of an adjustable-rate mortgage (ARM), but it offers the advantage of never changing.

With a fixed-rate mortgage, you can budget your finances more effectively because you know exactly how much your mortgage payment will be each month. This can be especially helpful for homeowners who prefer consistency and want to avoid any surprises in their monthly expenses.

Advantages of Fixed-rate Mortgages

One of the main advantages of a fixed-rate mortgage is the stability it provides. You don’t have to worry about your monthly mortgage payment fluctuating with market conditions or interest rate changes. This can be particularly beneficial if you have a fixed income or if you value the peace of mind that comes with knowing your payment won’t change.

Another advantage is that fixed-rate mortgages allow you to plan for the long-term. When you lock in a fixed interest rate, you can calculate exactly how much interest you will pay over the life of the loan. This can help you make informed decisions about your financial goals and when to pay off your mortgage.

Disadvantages of Fixed-rate Mortgages

One disadvantage of fixed-rate mortgages is that the initial interest rate tends to be higher compared to adjustable-rate mortgages. This means that your monthly payment may be higher initially, which could be a barrier for some borrowers, especially those with tighter budgets.

Additionally, if interest rates drop significantly after you have taken out a fixed-rate mortgage, you will not benefit from the lower rates unless you refinance your loan. Refinancing can be costly and time-consuming, so it’s important to consider whether you are comfortable with the possibility of missing out on lower interest rates over time.

Adjustable-rate Mortgages

Definition and Features of Adjustable-rate Mortgages

An adjustable-rate mortgage (ARM) is a type of home loan where the interest rate can fluctuate over time. The initial interest rate of an ARM is typically lower than that of a fixed-rate mortgage, making it an attractive option for borrowers who want to take advantage of lower rates in the beginning.

The interest rate on an ARM is linked to a financial index, such as the U.S. Treasury securities or the London Interbank Offered Rate (LIBOR). The rate is adjusted periodically, usually every one, three, five, or seven years, based on changes in the index. This means that your monthly mortgage payment can increase or decrease over the course of the loan.

Advantages of Adjustable-rate Mortgages

One of the main advantages of an adjustable-rate mortgage is the lower initial interest rate. If you are confident that interest rates will remain low for the foreseeable future, an ARM can be a cost-effective option, especially if you plan to sell the property or refinance before the interest rate adjusts.

Another advantage of ARMs is that they offer more flexibility compared to fixed-rate mortgages. If you anticipate a change in your income or plan to move in the near future, an ARM can provide you with a lower monthly payment during the initial fixed-rate period. This can be particularly beneficial if you expect your financial situation to improve or if you are considering selling the property before the adjustable-rate period begins.

Disadvantages of Adjustable-rate Mortgages

The main disadvantage of adjustable-rate mortgages is the uncertainty associated with interest rate fluctuations. Because the interest rate can change over time, your monthly mortgage payment can increase significantly, making it harder to budget and plan for your expenses. This can be a significant drawback for borrowers who prefer stability and want to avoid the risk of higher payments in the future.

Another disadvantage is that if interest rates rise significantly, your monthly payment could become unaffordable. It is important to carefully consider your ability to handle potential payment increases and assess your risk tolerance before opting for an ARM.

Factors to Consider

Current Market Conditions

When deciding between a fixed-rate and adjustable-rate mortgage, it is important to consider the current market conditions. If interest rates are low and expected to rise in the future, a fixed-rate mortgage may be a more favorable option. On the other hand, if interest rates are high and projected to decrease, an adjustable-rate mortgage may offer short-term savings.

Financial Goals and Stability

Consider your financial goals and stability when choosing between mortgage types. If you value stability and predictability, a fixed-rate mortgage can provide you with peace of mind. However, if you are comfortable with some uncertainty and want to take advantage of potential rate decreases, an adjustable-rate mortgage might be suitable for you.

Loan Duration and Risk Tolerance

Evaluate your loan duration and risk tolerance when making a decision. If you plan to stay in the property for a longer period of time and prefer consistency, a fixed-rate mortgage may be a better fit. However, if you anticipate a shorter-term stay or are comfortable with potential payment adjustments, an adjustable-rate mortgage may be more suitable.

Predictability of Monthly Payments

Consider how important predictable monthly payments are to you. With a fixed-rate mortgage, you will have the same monthly payment throughout the life of the loan. If you prefer knowing exactly how much you will pay each month, a fixed-rate mortgage is the way to go. However, if you are comfortable with fluctuations in your payments and can handle potential increases, an adjustable-rate mortgage may offer more flexibility.

Interest Rate Forecasts

Review interest rate forecasts to make an informed decision. Research and analyze expert opinions and projections on future interest rates. While no one can predict the future with certainty, understanding the trends and potential changes can help guide your decision-making process.

Comparison of Fixed-rate and Adjustable-rate Mortgages

Interest Rate Stability

A fixed-rate mortgage offers interest rate stability since the rate remains the same for the entire loan term. This means your monthly payments will not change. On the other hand, an adjustable-rate mortgage offers initial stability followed by potential rate adjustments. The stability or fluctuation of the interest rate depends on the market conditions and the terms of the loan.

Monthly Payment Stability

With a fixed-rate mortgage, your monthly payment remains constant throughout the life of the loan. This can provide peace of mind, especially for budget-conscious individuals. On the other hand, with an adjustable-rate mortgage, your monthly payment can change periodically, depending on the interest rate adjustments. This can lead to uncertainty and potential increased expenses.

Initial Interest Rate

The initial interest rate of an adjustable-rate mortgage is typically lower than that of a fixed-rate mortgage. This can result in lower monthly payments during the initial fixed-rate period. However, it is essential to consider how this initial lower rate might change over time and the potential impact on your budget.

Future Rate Adjustments

With an adjustable-rate mortgage, the interest rate can adjust periodically after the initial fixed-rate period ends. Factors such as market conditions and the terms of the loan will determine how often the rate adjusts and by how much. This can impact your monthly payments and overall costs.

Loan Term Options

Both fixed-rate and adjustable-rate mortgages offer different loan term options. Fixed-rate mortgages often come in 15-year or 30-year terms, allowing you to choose the best duration for your financial goals. Adjustable-rate mortgages may offer a fixed rate for a shorter initial period, such as three, five, or seven years, before the interest rate adjusts. Consider which loan term aligns with your long-term plans.

This image is property of www.mortgagecalculator.org.

When to Choose a Fixed-rate Mortgage

Prefer Predictable Payments

If you prefer the peace of mind that comes with knowing your monthly mortgage payment will never change, a fixed-rate mortgage is an excellent choice for you. Whether you are on a tight budget or simply value consistency, a fixed-rate mortgage can provide the stability you desire.

Current Interest Rates are Low

When interest rates are low, it may be a good time to consider a fixed-rate mortgage. Locking in a low rate can help you save money over the life of the loan, especially if rates are expected to rise in the future. However, it’s important to carefully evaluate your financial situation and compare the costs of fixed-rate and adjustable-rate mortgages.

Long-term Stay in the Property

If you plan to stay in your property for the long term, a fixed-rate mortgage can be a suitable option. You will have the security of a set monthly payment for the entire loan term, regardless of changes in the market or future interest rate fluctuations.

Risk Averse Borrowers

If you are risk-averse and prefer to avoid uncertainties with fluctuating interest rates, a fixed-rate mortgage is the ideal choice. It provides the stability you need without being exposed to the potential downsides of adjustable-rate mortgages.

When to Choose an Adjustable-rate Mortgage

Expecting Interest Rates to Drop

If interest rates are currently high but expected to drop in the future, an adjustable-rate mortgage can be advantageous. The initial lower interest rate can provide short-term savings, especially if you plan to sell or refinance before the adjustable-rate period begins.

Short-term Stay in the Property

If you anticipate a short-term stay in the property, an adjustable-rate mortgage can be a suitable option. During the initial fixed-rate period, you can enjoy lower monthly payments without worrying about potential interest rate increases. This can be beneficial if you plan to sell the property or refinance before the adjustable-rate period begins.

Ability to Handle Potential Payment Increases

If you have the financial flexibility to handle potential payment increases in the future, an adjustable-rate mortgage can offer more flexibility and potential savings during the initial fixed-rate period. It’s important to assess your risk tolerance and ensure that potential payment adjustments will not put a strain on your budget.

Flexibility in Paying Off the Mortgage

If you value flexibility in paying off your mortgage, an adjustable-rate mortgage may be suitable. You can take advantage of the lower initial interest rate to make additional principal payments and potentially pay off your loan faster. This can be beneficial for borrowers who have the financial means to pay more towards their mortgage during the initial fixed-rate period.

This image is property of www.mortgagecalculator.org.

Risks and Considerations

Possible Impact of Interest Rate Changes

One of the main risks associated with adjustable-rate mortgages is the possibility of interest rate increases over time. If interest rates rise significantly, your monthly mortgage payment can become unaffordable, causing financial stress. It is crucial to carefully consider your ability to handle payment increases before opting for an adjustable-rate mortgage.

Hidden Costs and Fees

When comparing fixed-rate and adjustable-rate mortgages, it’s important to take into account the hidden costs and fees associated with each. Consider closing costs, origination fees, and any potential penalties or charges for early repayment or refinancing. These additional costs can impact the overall affordability of the loan.

Qualification Criteria and Risks

Qualifying for an adjustable-rate mortgage may differ from qualifying for a fixed-rate mortgage. Lenders may have specific criteria and requirements for borrowers, including credit score, income verification, and debt-to-income ratio. It’s essential to understand the qualification process and the potential risks involved before making a decision.

Refinancing Options

If you choose an adjustable-rate mortgage, it’s important to consider your refinancing options. If interest rates rise significantly or you want to switch to a fixed-rate mortgage, you may need to refinance your loan. However, refinancing can come with additional costs, so it’s crucial to carefully evaluate the potential benefits and drawbacks.

Shopping for Mortgages and Comparing Offers

Interest Rates and Loan Terms

When shopping for mortgages, compare interest rates and loan terms from different lenders. Even a small difference in interest rates can have a significant impact on the overall cost of the loan. Additionally, consider the duration of the loan and choose the term that aligns with your financial goals.

Closing Costs and Additional Fees

Look out for closing costs and additional fees associated with the mortgage. It’s crucial to understand the breakdown of costs and factor them into your decision-making process. Compare the closing costs and fees offered by different lenders to find the most cost-effective option.

Types of Lenders

Consider the types of lenders available and choose the one that suits your needs. You can choose between traditional banks, credit unions, mortgage brokers, or online lenders. Each type of lender may have different rates, terms, and qualification requirements, so it’s important to explore your options.

Loan Documentation

Review the required loan documentation from different lenders. Lenders may have different document requirements and verification processes. Ensure that you are comfortable with the documentation process and gather all the necessary paperwork to avoid any delays or complications.

Pre-approval Process

Consider getting pre-approved for a mortgage before shopping around. Pre-approval can help you understand how much you can borrow and provide you with a stronger position when negotiating with sellers. It also gives you an idea of the interest rates and terms you may qualify for, helping you make a more informed decision.

Negotiating and Locking in Rates

Once you have identified a suitable lender, consider negotiating the terms of your mortgage. You may be able to negotiate the interest rate, closing costs, or other fees. Additionally, consider locking in your interest rate to protect against potential rate increases before closing on the loan.

This image is property of www.thetruthaboutmortgage.com.

Case Studies and Examples

Scenario 1: Stable Interest Rates

In a scenario where interest rates are stable and expected to remain so, a fixed-rate mortgage might be the preferred choice. Homeowners can budget with confidence, knowing their monthly mortgage payments will not change. This is suitable for individuals seeking stability and predictable expenses.

Scenario 2: Fluctuating Interest Rates

If interest rates are currently high but expected to decrease, an adjustable-rate mortgage may offer short-term savings. Homeowners can take advantage of the initial lower interest rate, especially if they plan to sell or refinance before the rate adjusts. However, it’s essential to carefully consider the potential risks of future rate increases.

Scenario 3: Short-term Investment Property

For individuals purchasing a property for short-term investment purposes, an adjustable-rate mortgage offers flexibility. During the initial fixed-rate period, borrowers can benefit from lower monthly payments before potentially selling the property. This scenario aligns with individuals who plan to capitalize on short-term gains.

Scenario 4: Long-term Residence

For homeowners intending to stay in the property for the long term, a fixed-rate mortgage provides stability and security. Monthly payments will remain the same for the entire loan term, allowing homeowners to plan their finances with certainty. This scenario suits those seeking consistency and avoiding the risk of future payment increases.

Conclusion

Choosing a mortgage is a significant decision that should be based on careful evaluation of your financial circumstances and goals. Fixed-rate mortgages offer stability and predictability, making them ideal for risk-averse borrowers and those looking for consistent monthly payments. On the other hand, adjustable-rate mortgages provide flexibility, potential short-term savings, and opportunities for those expecting interest rates to drop or with short-term residence plans.

Consider the current market conditions, your financial goals, and projected stability, as well as your risk tolerance before making a decision. Remember to factor in future interest rate adjustments, loan term options, and hidden costs associated with each type of mortgage. Shopping around for the best rates, terms, and lender options is essential in finding the mortgage that suits your individual needs.

By thoroughly considering your circumstances and comparing the advantages and disadvantages of fixed-rate and adjustable-rate mortgages, you can make an informed decision that aligns with your financial goals and provides you with long-term satisfaction as a homeowner.

This image is property of www.mortgagecalculator.org.