Are you considering whether to lease or loan a car? It’s a big decision, and understanding the pros and cons of each option can help you make the right choice. Leasing a car can offer lower monthly payments and the opportunity to drive a new vehicle every few years, but it also comes with mileage restrictions and no ownership at the end of the term. On the other hand, loaning a car allows you to build equity and have the freedom to customize your vehicle, but it typically involves higher monthly payments and the responsibility of maintenance costs. In this article, we will explore the pros and cons of leasing versus loaning a car, so you can make an informed decision that suits your needs and preferences.

This image is property of www.investopedia.com.

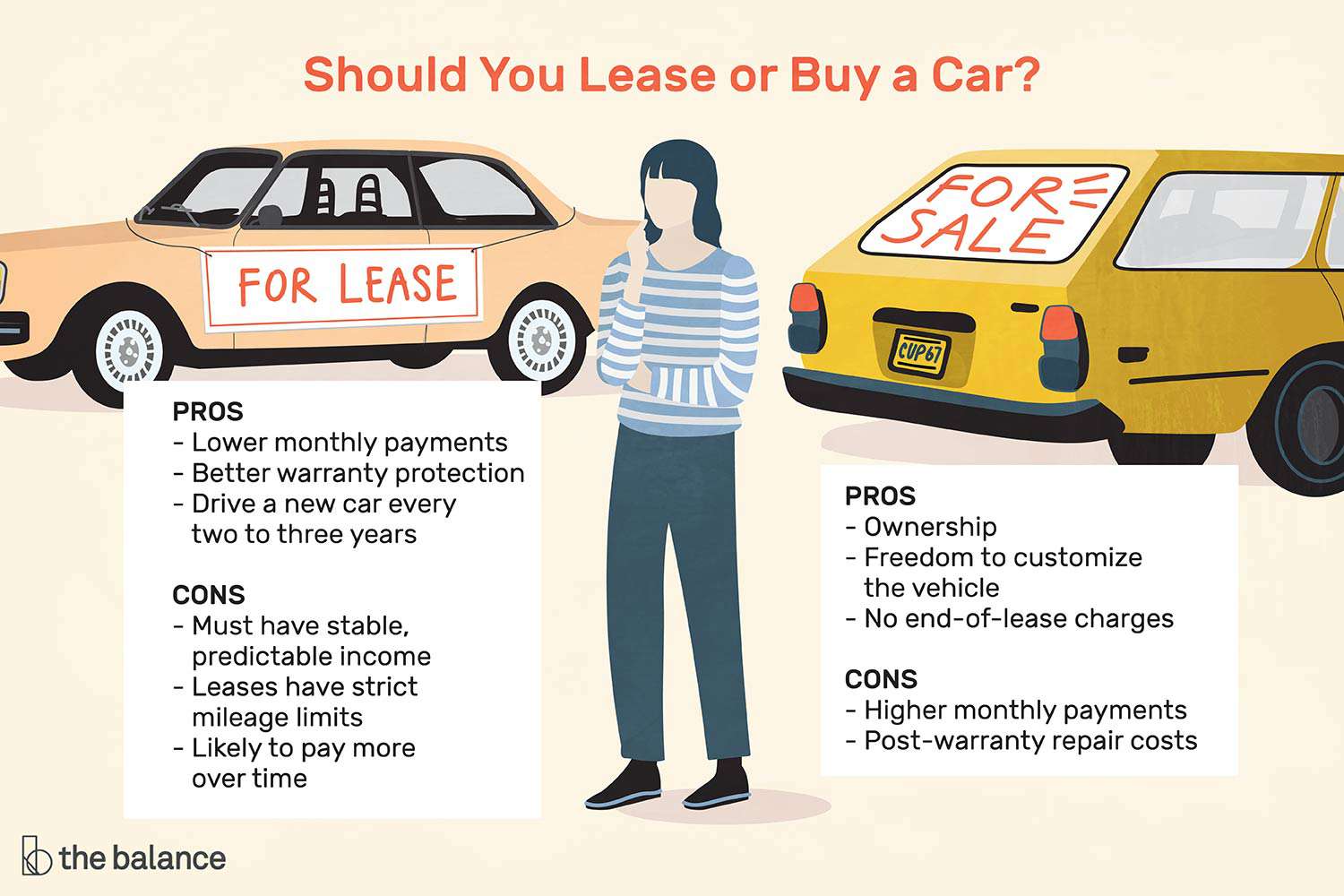

Leasing a Car

Leasing a car is a popular option for many people, and it comes with several benefits. Let’s take a look at some of the advantages you can enjoy when you choose to lease a car.

Lower Monthly Payments

One of the main advantages of leasing a car is the lower monthly payments. When you lease a car, you are essentially paying for the depreciation of the vehicle during the lease term, rather than the full cost of the car. This can result in significantly lower monthly payments compared to if you were to take out a loan to purchase the car.

Less Money Down

In addition to lower monthly payments, leasing a car often requires less money down compared to financing a car with a loan. When you lease a car, you typically only need to make a small initial payment, sometimes referred to as a “drive-off” fee. This can be a great advantage for those who don’t have a large amount of cash on hand to put down on a vehicle.

Vehicle Variety

Another benefit of leasing a car is the opportunity to drive a new vehicle every few years. Since leases typically last for a few years, you have the chance to experience the latest models and upgrades without the commitment of ownership. This can be particularly appealing to those who enjoy having the latest features and technology in their vehicles.

Warranty Coverage

When you lease a car, it often comes with a manufacturer’s warranty. This means that any repairs or maintenance needed during the lease term may be covered by the warranty, resulting in lower out-of-pocket costs for you. Having warranty coverage can provide peace of mind and protect you from unexpected expenses.

Lower Maintenance Costs

Leasing a car can also result in lower maintenance costs. Since leased vehicles are typically new or only a few years old, they are less likely to require major repairs. Additionally, routine maintenance may be covered by the warranty, further reducing your expenses. With lower maintenance costs, you can save money and enjoy a worry-free driving experience.

Loaning a Car

While leasing a car has its advantages, there are also benefits to consider when it comes to loaning a car through financing. Let’s explore some of the advantages of taking out a car loan.

Ownership

When you finance a car through a loan, you become the owner of the vehicle. This means that once the loan is paid off, you will have full ownership of the car. Owning a car can provide a sense of security and flexibility, as you have the freedom to modify or sell the vehicle as you please.

Equity Buildup

One of the advantages of loaning a car is the opportunity to build equity. As you make monthly payments towards your car loan, you are gradually paying off the principal amount borrowed. This can result in the buildup of equity in the vehicle, which can be beneficial if you plan to sell or trade-in the car in the future.

Customization

When you own a car, you have the freedom to customize it according to your preferences. Whether it’s adding new features, upgrading the sound system, or changing the paint color, owning a car allows you to personalize it to your liking. This level of customization is not typically possible with leased vehicles, as modifications are often restricted.

Mileage Limitations

One consideration when loaning a car is the freedom to drive without mileage restrictions. Unlike leasing, where there are typically mileage limitations, owning a car allows you to drive as much as you want without incurring additional fees. If you have a long commute or enjoy taking road trips, owning a car may be a more suitable option for you.

Higher Monthly Payments

While leasing a car often comes with lower monthly payments, loaning a car generally results in higher monthly payments. This is because you are financing the full cost of the car, without the benefit of paying only for the depreciation. It’s important to consider your budget and financial situation when deciding between leasing and loaning a car.

Comparing Costs

When it comes to the cost of leasing versus loaning a car, it’s essential to consider both upfront costs and long-term expenses. Let’s explore these factors in more detail.

Upfront Costs

Leasing a car typically requires less money down compared to financing a car through a loan. The upfront costs for a lease are usually limited to the first month’s payment, a security deposit, a small initial payment, and any applicable fees. On the other hand, loaning a car often requires a significant down payment, which can include sales tax, registration fees, and other expenses.

Monthly Payments

As mentioned earlier, leasing a car often comes with lower monthly payments compared to loaning a car. This is because you are only paying for the depreciation of the vehicle during the lease term, rather than the full cost of the car. On the other hand, loaning a car requires higher monthly payments since you are financing the entire purchase price.

Long-term Expenses

When comparing the long-term expenses of leasing versus loaning a car, it’s important to consider factors such as maintenance costs, insurance rates, and potential savings. Leased vehicles often come with warranty coverage, which can help reduce maintenance costs. On the other hand, owned vehicles may require more significant repairs as they age, resulting in higher out-of-pocket expenses. Additionally, insurance rates can vary depending on the type of vehicle and ownership status.

Financial Considerations

Before deciding whether to lease or loan a car, it’s crucial to consider the financial implications of each option. Let’s explore some of the key financial considerations you should keep in mind.

Credit Requirements

Both leasing and loaning a car require credit approval, but the credit requirements may differ between the two options. Leasing may have more flexible credit requirements, as the lender is primarily concerned with your ability to make monthly payments. Loaning a car, on the other hand, often requires a higher credit score and may have stricter lending criteria.

Credit Score Impact

Another financial consideration is the impact on your credit score. Leasing a car may have a minimal impact on your credit score, as long as you make your payments on time. Loaning a car, on the other hand, can have a positive impact on your credit score if you make your payments consistently and on time. However, missed or late payments can negatively affect your credit score.

Interest Rates

The interest rates for leasing and loaning a car can vary. When leasing a car, you are essentially renting the vehicle, so the interest rates may be lower compared to financing a car through a loan. Loan interest rates, on the other hand, can depend on various factors, including your credit score, the length of the loan, and the lender’s policies. It’s important to compare interest rates and loan terms to determine the most cost-effective option for you.

This image is property of www.thebalancemoney.com.

Potential Savings

When considering whether to lease or loan a car, it’s essential to evaluate the potential savings associated with each option. Let’s take a look at some of the potential savings you can enjoy with each choice.

Resale Value

Owning a car can provide the opportunity to benefit from its resale value. As the owner, you have the option to sell or trade-in the vehicle at any time. Depending on factors such as the make, model, mileage, and overall condition of the car, you may be able to recoup a significant portion of your investment. This potential for resale value can be a valuable savings opportunity.

Tax Benefits

Both leasing and loaning a car can offer certain tax benefits, though they can differ based on your personal circumstances. When leasing a car for business purposes, you may be eligible for tax deductions on your lease payments. On the other hand, loaning a car may provide tax benefits in terms of depreciating the vehicle’s value over time. It’s important to consult with a tax professional to determine the specific tax advantages applicable to your situation.

Insurance Rates

Insurance rates can also play a role in potential savings when leasing or loaning a car. Leased vehicles often come with more comprehensive coverage options, which can result in higher insurance rates. On the other hand, owned vehicles may offer more flexibility in choosing insurance coverage and potentially lower insurance premiums. Comparing insurance quotes for both leasing and loaning scenarios can help you identify potential savings in this area.

Flexibility and Restrictions

When it comes to flexibility and restrictions, there are important considerations to keep in mind when deciding between leasing and loaning a car. Let’s explore these factors in more detail.

Lease Termination

Leasing a car comes with a predetermined lease term, typically lasting a few years. While this can be advantageous for those who enjoy driving a new vehicle every few years, it also means that terminating a lease early can come with penalties. Additionally, exceeding the mileage limit or not maintaining the car according to the lease terms can result in additional charges. It’s important to be aware of these potential restrictions when considering leasing a car.

Loan Duration

When you finance a car through a loan, the loan duration can vary based on your chosen loan term. This flexibility can be advantageous for those who prefer to have a more extended period of ownership without the need to enter into a new lease agreement. However, it’s important to consider the financial implications of a longer loan duration, such as the potential for higher interest payments and extended financial commitments.

Usage Limitations

Leasing a car often comes with mileage limitations, which can restrict your driving habits. Exceeding the mileage limit specified in the lease agreement can result in additional fees. Loaning a car, on the other hand, does not typically come with mileage limitations, allowing you to drive as much as you want without incurring additional charges. If you have a long commute or frequently travel long distances, owning a car may provide more flexibility in terms of usage.

Modifications

Leased vehicles often come with restrictions on modifications. The lease agreement may prohibit any alterations to the vehicle, such as adding aftermarket parts or making cosmetic changes. Ownership, on the other hand, provides the freedom to modify the car as desired. If you enjoy customizing your vehicle or plan to make modifications in the future, owning a car may be the more suitable option for you.

This image is property of i.insider.com.

Long-Term Goals

Considering your long-term goals is crucial when deciding between leasing and loaning a car. Let’s explore some of the long-term factors you should consider.

Ownership Satisfaction

Owning a car can provide a sense of pride and satisfaction. If you value the ownership experience and the freedom that comes with it, loaning a car may be the better choice for you. Being the owner of a vehicle allows you to develop a long-term relationship with your car and potentially build equity over time.

Trade-in Value

When you own a car, you have the opportunity to benefit from its trade-in value. As mentioned earlier, owned vehicles can be sold or traded-in, allowing you to recoup a portion of your investment. This trade-in value can be advantageous when it comes time to upgrade to a new vehicle.

Future Financial Flexibility

Considering your future financial flexibility is also important. Leasing a car often provides lower monthly payments, allowing you to allocate your funds towards other financial goals such as saving for a down payment on a home or investing. On the other hand, loaning a car may provide greater financial flexibility in the long run, as you have the option to sell or trade-in the vehicle and potentially recoup a significant portion of your investment.

Considerations for Business Use

If you are considering leasing or loaning a car for business use, there are specific considerations to keep in mind. Let’s explore these factors in more detail.

Tax Deductions

Leasing a car for business purposes can offer certain tax deductions. The IRS allows you to deduct a portion of your lease payments if the vehicle is used for business purposes. This can result in potential tax savings for your business. It’s important to consult with a tax professional to understand the specific tax implications and eligibility criteria for business lease deductions.

Depreciation

When you own a car for business use, you can potentially benefit from depreciation deductions. The IRS allows you to deduct a portion of the vehicle’s depreciation as a business expense. This depreciation deduction can result in tax savings for your business over time. It’s important to consult with a tax professional to determine the specific depreciation deductions applicable to your business.

Lease vs. Loan Decision

When it comes to business use, the decision between leasing and loaning a car depends on several factors, including your business needs, financial goals, and tax considerations. Leasing may provide lower monthly payments and tax deductions, making it a suitable option for businesses that prefer to have access to newer vehicles without the long-term commitment. Loaning a car can offer the opportunity to build equity, claim depreciation deductions, and potentially save on interest payments. It’s important to consider these factors and consult with a financial advisor or tax professional to make an informed decision for your business.

This image is property of napkinfinance.com.

Maintenance and Repairs

Considering the costs associated with maintenance and repairs is essential when deciding between leasing and loaning a car. Let’s discuss these factors in more detail.

Warranty Coverage

Leased vehicles often come with warranty coverage, which can help reduce maintenance and repair costs. The manufacturer’s warranty may cover certain repairs and routine maintenance during the lease term, potentially resulting in lower out-of-pocket expenses. On the other hand, when you own a car, warranty coverage may expire, and you may be responsible for all maintenance and repair costs. It’s important to factor in these costs when considering leasing or loaning a car.

Routine Maintenance

Regardless of whether you lease or own a car, routine maintenance is essential to keep the vehicle in good condition. This includes regular oil changes, tire rotations, and other scheduled maintenance tasks. Leased vehicles may come with a maintenance package that covers these routine services, while owned vehicles require you to bear the full cost of maintenance. It’s crucial to consider your budget and maintenance needs when deciding between leasing and loaning a car.

Out-of-Warranty Costs

When you lease a car, any repairs or maintenance needed outside of the warranty coverage may result in additional expenses. These out-of-warranty costs can vary depending on the extent of the repairs and the specific vehicle. On the other hand, when you own a car, you are responsible for all maintenance and repair costs, including both routine and more significant repairs. It’s important to budget for these potential expenses when making your decision.

Conclusion

When it comes to deciding whether to lease or loan a car, it’s important to consider your individual circumstances, preferences, and financial goals. Leasing a car offers lower monthly payments, less money down, and the opportunity to drive a new vehicle every few years. On the other hand, loaning a car provides ownership, equity buildup, customization options, and potentially lower long-term expenses. By carefully considering the advantages and potential drawbacks of each option, you can make an informed decision that aligns with your needs and priorities. Remember to evaluate factors such as upfront costs, monthly payments, long-term expenses, financial considerations, potential savings, flexibility and restrictions, long-term goals, considerations for business use, and maintenance and repair costs. Ultimately, choosing the right option for you will depend on factors such as your budget, driving habits, future plans, and personal preferences.

This image is property of i.insider.com.