In the world of mortgages, jumbo loans have been increasingly gaining popularity. As property prices continue to rise, more and more homebuyers are turning to jumbo loans to finance their dream homes. However, securing a jumbo loan is no easy feat, as strict requirements and higher down payments come into play. This article explores the rise of jumbo loans, delving into their requirements and shedding light on the factors that have contributed to their surging popularity. Whether you’re a potential borrower or simply curious about the shifting landscape of home financing, this article will provide valuable insights into the world of jumbo loans.

What are Jumbo Loans?

Definition of Jumbo Loans

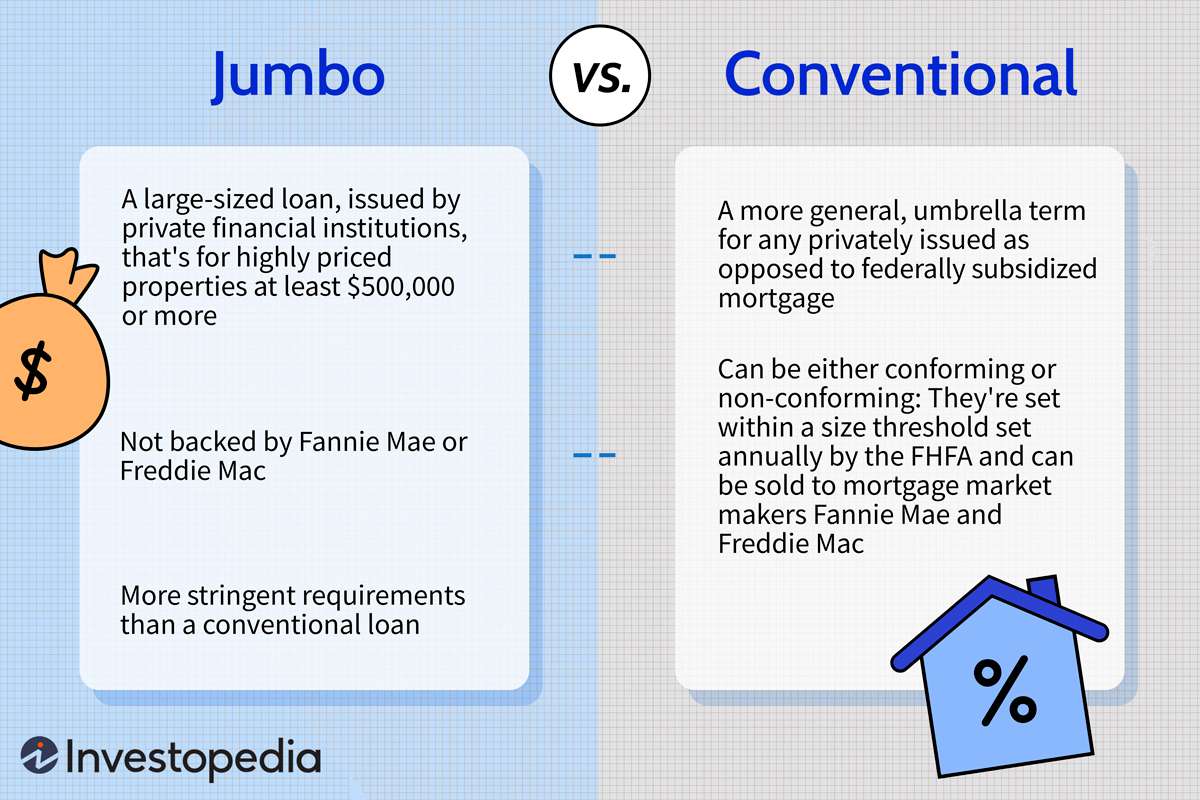

Jumbo loans, also known as non-conforming loans, are mortgage loans that exceed the conforming loan limits set by government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac. These loans are designed for borrowers purchasing or refinancing high-value properties that cost more than the conventional loan limits. In general, any loan amount above $548,250 (as of 2021) is considered a jumbo loan, although this may vary depending on the region.

Comparison to Conventional Loans

The main difference between jumbo loans and conventional loans is the loan amount. Conventional loans adhere to the conforming loan limits set by GSEs and are typically easier to qualify for, with lower credit score and down payment requirements. Jumbo loans, on the other hand, are for larger loan amounts and often require higher credit scores, larger down payments, and a more rigorous approval process. While both options provide borrowers with the opportunity to finance their dream homes, jumbo loans are specifically tailored to meet the needs of high-net-worth individuals.

The Growth of Jumbo Loans

Reasons for the Increase

In recent years, jumbo loans have experienced significant growth in popularity. Several factors contribute to this trend. Firstly, a surge in real estate prices has led to an increased demand for luxury properties. As housing markets continue to thrive, borrowers are seeking financing options that accommodate the higher costs associated with these premium homes. Additionally, historically low interest rates have made jumbo loans more attractive, as borrowers can secure financing at competitive rates. Finally, the rise in incomes and wealth among affluent individuals has fueled the demand for jumbo loans, as more borrowers have the financial means to afford luxury properties.

Impact on Real Estate Market

The rise of jumbo loans has had a profound impact on the real estate market. As more borrowers seek financing for high-value properties, the availability of jumbo loans increases housing affordability for those interested in purchasing luxury homes. This stimulates the overall growth of the real estate market and contributes to the appreciation of property values. However, the increased demand for jumbo loans can also lead to price inflation in certain geographic areas, making it more challenging for some buyers to enter the market.

This image is property of www.investopedia.com.

Requirements for Jumbo Loans

Higher Credit Score

To qualify for a jumbo loan, borrowers typically need a higher credit score compared to conventional loans. Lenders consider credit history and credit scores as indicators of a borrower’s financial responsibility and ability to manage larger loan amounts. While the specific credit score requirements may vary among lenders, a score of 700 or higher is generally considered a favorable starting point for jumbo loan eligibility.

Greater Down Payment

Jumbo loans often require a larger down payment compared to conventional loans. This is because lenders bear a higher level of risk when financing larger loan amounts. While conventional loans may allow down payments as low as 3% to 5% of the purchase price, jumbo loans may require a minimum down payment of 20% or more. A larger down payment not only reduces the lender’s risk but also demonstrates the borrower’s financial stability and commitment to the loan.

Debt-to-Income Ratio

Lenders closely evaluate a borrower’s debt-to-income (DTI) ratio when considering jumbo loan applications. The DTI ratio represents the percentage of a borrower’s monthly gross income that goes toward paying off debts, including the proposed jumbo loan. Typically, lenders prefer a DTI ratio of 43% or lower for jumbo loans. This ensures that borrowers have sufficient income to cover their existing debt obligations while comfortably making payments on the jumbo loan.

Reserve Requirements

In addition to a higher credit score, larger down payment, and favorable DTI ratio, jumbo loan borrowers may be subject to reserve requirements. Reserves refer to the amount of liquid assets, such as cash or investment accounts, that a borrower has available after closing on the loan. These reserves act as a safety net, assuring lenders that borrowers have the financial capability to handle unexpected expenses or a loss of income. Typically, lenders require borrowers to have several months’ worth of mortgage payments in reserves, although this requirement can vary depending on individual circumstances.

Jumbo Loan Limits

Federal Regulations

Jumbo loan limits are determined by federal regulations and are subject to periodic adjustments. In most areas of the United States, the jumbo loan limit is set at $548,250 for 2021. However, in high-cost regions where housing prices are significantly higher, such as certain metropolitan areas, the jumbo loan limit may be higher to accommodate the local market conditions. It is crucial for borrowers to consult with lenders or mortgage professionals to determine the specific loan limits in their area.

Regional Variations

While federal regulations set the baseline for jumbo loan limits, there are regional variations that borrowers should be aware of. Certain high-cost areas, such as San Francisco or New York City, may have significantly higher jumbo loan limits due to the exorbitant housing prices in those regions. It is important for borrowers to research and understand the jumbo loan limits specific to their desired property location, as it can significantly impact the financing options available to them.

This image is property of blog.mint.com.

Advantages of Jumbo Loans

Financing High-Value Properties

One of the primary advantages of jumbo loans is the ability to finance high-value properties. Conventional loans often have limitations on loan amounts, making it challenging for borrowers to secure financing for luxury homes. Jumbo loans bridge this gap, allowing borrowers to purchase or refinance their dream homes regardless of the property’s price tag. This flexibility provides borrowers with the opportunity to invest in prestigious properties that align with their lifestyle and financial goals.

Flexible Mortgage Options

Jumbo loans offer a range of mortgage options tailored to meet the unique needs of borrowers. From fixed-rate jumbo loans to adjustable-rate and interest-only options, borrowers can choose the loan structure that aligns with their financial preferences and long-term plans. This flexibility allows borrowers to customize their mortgage terms to suit their current financial situation while taking advantage of favorable interest rates or repayment plans.

Disadvantages of Jumbo Loans

Higher Interest Rates

One of the disadvantages of jumbo loans is that they often carry higher interest rates compared to conventional loans. Because jumbo loans involve larger loan amounts and increased risk for lenders, they typically come with higher interest charges to compensate for this risk. Borrowers should carefully consider the long-term financial implications of higher interest rates and assess whether the benefits of jumbo loans outweigh the potential costs.

Stricter Approval Process

Obtaining approval for a jumbo loan can be more challenging and time-consuming compared to conventional loans. Lenders assess jumbo loan applications more thoroughly due to the larger loan amounts and increased risk involved. The approval process may require additional documentation, such as extensive financial records, proof of income, and asset verification, to ensure borrowers meet the stringent criteria. Prospective jumbo loan borrowers should be prepared for a more rigorous and potentially lengthier approval process.

This image is property of www.investopedia.com.

How to Qualify for a Jumbo Loan

Improving Credit Score

To improve your chances of qualifying for a jumbo loan, focusing on improving your credit score is crucial. Paying bills on time, reducing credit card balances, and minimizing new credit applications can positively impact your credit score over time. Regularly reviewing your credit report for inaccuracies and addressing any issues promptly can also help boost your creditworthiness and increase your chances of meeting the credit score requirements.

Saving for a Larger Down Payment

Jumbo loans often require a larger down payment, so it is essential to save diligently to meet this requirement. Consider creating a budget and cutting back on unnecessary expenses to accelerate your savings. Explore different savings options such as high-yield savings accounts or investment vehicles to maximize the returns on your savings. A larger down payment not only increases your chances of loan approval but also reduces the loan amount, potentially lowering your monthly mortgage payments.

Reducing Other Debts

Lenders carefully evaluate the debt-to-income ratio when considering jumbo loan applications. To improve your DTI ratio, focus on reducing your existing debts. Paying off high-interest debts or consolidating them into more manageable loans can help lower your monthly debt obligations, thereby improving your overall financial profile. By reducing other debts, you can free up more of your income to demonstrate your ability to comfortably handle the jumbo loan payments.

Jumbo Loan vs. Conventional Loan

Loan Amount

The primary difference between jumbo loans and conventional loans is the loan amount. Conventional loans adhere to the conforming loan limits set by GSEs, while jumbo loans exceed these limits. Conventional loans are suitable for borrowers purchasing properties within the conforming loan limits, while jumbo loans are tailored for borrowers seeking financing for high-value properties.

Interest Rates

Jumbo loans often carry higher interest rates compared to conventional loans due to the increased risk involved. Conventional loans benefit from the backing of GSEs, which lowers the perceived risk for lenders. However, jumbo loans typically do not have this added layer of security, leading to higher interest charges to compensate for the higher risk.

Documentation Requirements

Jumbo loans typically require more extensive documentation compared to conventional loans. In addition to the standard documentation required for conventional loan applications, such as income verification and credit history, jumbo loans often require additional financial records. These may include tax returns, bank statements, and detailed proof of assets and liabilities. The comprehensive documentation requirement ensures that lenders have a complete understanding of a borrower’s financial situation before approving a jumbo loan.

This image is property of i0.wp.com.

Different Types of Jumbo Loans

Fixed-Rate Jumbo Loans

Fixed-rate jumbo loans offer borrowers the stability of a fixed interest rate throughout the loan term, typically ranging from 15 to 30 years. This means that the interest rate and monthly mortgage payments remain constant, providing borrowers with predictability and peace of mind. Fixed-rate jumbo loans are an excellent choice for those looking for long-term financial stability and prefer consistent mortgage payments.

Adjustable-Rate Jumbo Loans

Adjustable-rate jumbo loans, also known as ARMs, have interest rates that fluctuate based on market conditions. These loans typically have an initial fixed-rate period, followed by periodic adjustments. The initial fixed-rate period may vary, commonly ranging from 3 to 10 years. After the initial period, the interest rate adjusts periodically based on an index, such as the London Interbank Offered Rate (LIBOR). Adjustable-rate jumbo loans offer borrowers the opportunity to take advantage of potentially lower interest rates during the initial fixed-rate period.

Interest-Only Jumbo Loans

Interest-only jumbo loans allow borrowers to make interest-only payments for a specified period, typically ranging from 5 to 10 years. During this period, borrowers are not required to make principal payments, reducing their monthly mortgage obligations. After the interest-only period ends, the loan converts to a fully amortizing loan, and borrowers must start paying both principal and interest. Interest-only jumbo loans are suitable for borrowers who anticipate increased cash flow in the future or prefer lower monthly payments during the initial years of homeownership.

Obtaining a Jumbo Loan

Finding a Lender

Finding a lender specializing in jumbo loans is essential when seeking financing for a high-value property. Research various lenders, including banks, credit unions, and mortgage lenders, to compare their jumbo loan offerings, interest rates, and customer reviews. Work with a lender experienced in jumbo loans who can guide you through the application process and provide valuable insights on market conditions and loan options.

Meeting Application Criteria

To be considered for a jumbo loan, borrowers must meet the specific application criteria set by the lender. This typically includes demonstrating a strong credit history, having a substantial down payment, maintaining a favorable debt-to-income ratio, and providing the necessary financial documentation. Be prepared to provide extensive documentation to prove your financial stability and repayment capability.

Completing the Loan Application Process

The loan application process for jumbo loans is similar to that of conventional loans, with some additional steps. Gather all the required documentation, including income verification, tax returns, bank statements, and proof of assets and liabilities. Work closely with your lender to complete the application accurately and efficiently. Be prepared for a potentially longer processing time due to the more rigorous approval process associated with jumbo loans.

In conclusion, jumbo loans play a crucial role in financing high-value properties, enabling borrowers to fulfill their homeownership dreams. While they come with higher credit score requirements, larger down payments, and stricter approval processes, jumbo loans provide borrowers with flexible mortgage options and the opportunity to invest in luxury properties. By understanding the requirements, qualifying criteria, and various types of jumbo loans available, borrowers can navigate the jumbo loan process with confidence and secure the financing needed for their dream home.

This image is property of www.wallstreetmojo.com.