Are you drowning in student loan debt? It’s a common issue that millions of borrowers face after graduating from higher education. But what if there was a way to alleviate this burden and give borrowers a fresh start? That’s where the concept of forgiving student loans comes into play. This article explores the various aspects surrounding student loan forgiveness, including federal and private loans, debt relief options, eligibility criteria, repayment plans, and even tax implications. So, if you’re tired of being weighed down by your student loans, keep reading to find out more about this potential solution that could change your financial future.

How To Access Up To One Million Dollars Without Any Proof Of Income

Student Loan Forgiveness

If you are burdened by student loan debt, you may have heard about student loan forgiveness programs that can help you alleviate some or all of your debt. These programs are designed to provide relief to borrowers who are struggling to repay their loans due to financial hardship, low income, or other circumstances. In this comprehensive article, we will explore the different types of student loan forgiveness, eligibility criteria, application processes, and more. Whether you have federal or private loans, there may be options available to help you manage and potentially eliminate your student debt.

Federal Loan Forgiveness

Federal loan forgiveness programs are offered by the government and are designed to provide relief to borrowers who have federal student loans. These programs typically require borrowers to meet specific eligibility criteria, such as working in certain occupations or serving in the public sector for a specified period of time. The two main federal loan forgiveness programs are Income-Driven Repayment Plans and Public Service Loan Forgiveness.

Private Loan Forgiveness

Unlike federal loan forgiveness programs, private loan forgiveness options are not as common or widely available. Private lenders have different terms and conditions for loan forgiveness, and it is important to carefully review your loan agreement to understand if any forgiveness options are available. Some private lenders may offer loan forgiveness in cases of extreme financial hardship or in exchange for specific actions, such as community service or working in a high-demand field. It is important to contact your loan servicer directly to inquire about any possible forgiveness options.

Debt Relief Programs

In addition to loan forgiveness, there are also debt relief programs that can help borrowers manage their student loan debt more effectively. These programs aim to provide borrowers with alternative repayment options, such as extended repayment terms, reduced interest rates, or income-driven repayment plans. Debt relief programs can help borrowers lower their monthly payments, making them more manageable and potentially reducing the overall amount of money paid over the life of the loan.

Income-Driven Repayment Options

If you are struggling to make your monthly loan payments, income-driven repayment options may be the solution for you. These plans are designed to adjust your monthly payments based on your income and family size, making them more affordable and manageable. There are several income-driven repayment plans available, including Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE).

Income-Driven Repayment Plans

Income-Driven Repayment Plans, as the name suggests, calculate your monthly loan payments based on a percentage of your discretionary income. Discretionary income is the amount of money you have left after subtracting your adjusted gross income and 150% of the poverty line for your family size. The specific percentage used to calculate payments varies depending on the plan you choose. IBR and PAYE plans typically cap your monthly payments at 10% of your discretionary income, while REPAYE plans cap it at 10% or 15% depending on whether you have undergraduate or graduate loans.

Public Service Loan Forgiveness

Public Service Loan Forgiveness (PSLF) is a federal loan forgiveness program designed for borrowers who work in the public sector, such as government or non-profit organizations. To qualify for PSLF, you must make 120 qualifying monthly payments while working full-time for a qualifying employer. Once you have made the required number of payments, you may be eligible to have the remaining balance on your direct loans forgiven.

Teacher Loan Forgiveness

If you are a teacher, there is a specific loan forgiveness program tailored to your profession. Teacher Loan Forgiveness is available for teachers who have been employed full-time for five consecutive years in a low-income school or educational service agency. Under this program, you may be eligible for loan forgiveness of up to $17,500 on your direct loans or FFEL Program loans.

This image is property of cdn.ramseysolutions.net.

How To Access Up To One Million Dollars Without Any Proof Of Income

Loan Discharge and Deferment

In certain situations, you may be eligible for loan discharge or deferment, which can temporarily suspend your loan payments or eliminate your debt altogether.

Loan Discharge Options

Loan discharge options are available in cases where your loans are discharged due to specific circumstances or conditions. The most common types of loan discharge include Total and Permanent Disability Discharge, Military Service Forgiveness, and Borrower Defense to Repayment.

Total and Permanent Disability Discharge provides loan forgiveness for borrowers who are totally and permanently disabled and are unable to engage in substantial gainful activity, either due to a physical or mental condition. Military Service Forgiveness offers loan forgiveness for members of the armed forces who have served on active duty in a designated combat zone. Borrower Defense to Repayment allows borrowers to seek loan forgiveness if their school engaged in misconduct or misled them in some way.

Deferment Options

Deferment allows borrowers to temporarily postpone their loan payments, typically due to financial hardship or other qualifying circumstances. During a deferment period, interest may continue to accrue on certain types of loans, such as unsubsidized federal loans. Common deferment options include economic hardship deferment, unemployment deferment, and deferment for graduate fellowship programs.

Loan Repayment Options

If you are not eligible for loan forgiveness or deferment but still struggling to make your monthly payments, there are various loan repayment options available to help you manage your debt effectively.

Repayment Plans

Repayment plans determine the amount and duration of your loan payments. There are multiple repayment plans available, and the specific options depend on the type of loan you have. Some common repayment plans include Standard Repayment, Extended Repayment, Graduated Repayment, and Income-Contingent Repayment. It is important to assess your financial situation and choose a repayment plan that aligns with your income and budget.

Loan Consolidation

Loan consolidation allows borrowers to combine multiple federal loans into a single loan, with one monthly payment. This can simplify the repayment process, especially if you have multiple loan servicers or loan types. However, it is important to note that loan consolidation may result in an extended repayment term, potentially increasing the overall interest paid over the life of the loan.

Interest Rate Options

Interest rates play a significant role in the total amount paid for your loan. Depending on the type of loan you have and the terms of your agreement, you may have different interest rate options available. For example, federal loans generally have fixed interest rates, meaning the interest rate remains the same throughout the life of the loan. Private loans, on the other hand, may offer fixed or variable interest rates. It is important to understand the interest rate options and choose the one that best fits your financial goals and circumstances.

This image is property of media.npr.org.

How To Access Up To One Million Dollars Without Any Proof Of Income

Eligibility Criteria

Eligibility criteria for student loan forgiveness vary depending on the specific program or option you are considering. While some programs have specific requirements, such as working in a certain occupation or serving in a particular sector, others may have more general eligibility criteria based on factors such as income and financial need.

Qualifying Criteria for Forgiveness

Examples of qualifying criteria for forgiveness may include working in public service, teaching in low-income schools, or participating in humanitarian or volunteer work. It is essential to carefully review the requirements for each forgiveness program to determine if you meet the eligibility criteria.

Income and Financial Requirements

Certain student loan forgiveness programs, like income-driven repayment plans and debt relief programs, take into account your income and financial circumstances when determining eligibility. Income-driven repayment plans, for instance, adjust your monthly payments based on the percentage of your discretionary income. Debt relief programs may consider your financial hardship and income level to determine if you qualify for reduced payments or other repayment options. Providing accurate information about your income and financial situation is crucial to assess your eligibility for these programs.

Special Loan Forgiveness Programs

In addition to the general loan forgiveness programs mentioned earlier, there are several special loan forgiveness programs available for specific circumstances or professions.

Total and Permanent Disability Discharge

Total and Permanent Disability Discharge offers loan forgiveness for borrowers who are totally and permanently disabled and unable to engage in substantial gainful activity. By providing documentation of your disability status, you may be eligible to have your loans discharged, relieving you of the financial burden associated with repayment.

Military Service Forgiveness

If you have served in the military on active duty in a designated combat zone, you may be eligible for loan forgiveness under the Military Service Forgiveness program. This program offers loan forgiveness for members of the armed forces who have served in combat zones such as Iraq or Afghanistan.

Borrower Defense to Repayment

Borrower Defense to Repayment allows borrowers to seek loan forgiveness if they believe they were misled or defrauded by their school. This program is designed to protect borrowers who were victims of deceptive practices or misrepresentation by their educational institutions.

Income-Based Repayment

Income-Based Repayment (IBR) is a repayment plan that calculates your monthly payments based on a percentage of your income and family size. If you have a high debt-to-income ratio and struggling to make your student loan payments, IBR may be a suitable option for you.

Pay As You Earn

Pay As You Earn (PAYE) is another income-driven repayment plan that caps your monthly loan payments at 10% of your discretionary income. This plan is designed to provide relief to borrowers with high student loan debt and low income.

Revised Pay As You Earn

Revised Pay As You Earn (REPAYE) is a repayment plan that also uses your income and family size to calculate your monthly payment, but with a cap of 10% or 15% of your discretionary income, depending on whether you have undergraduate or graduate loans. REPAYE offers loan forgiveness after 20 or 25 years of qualifying payments, depending on your loan type.

This image is property of www.nysut.org.

How To Access Up To One Million Dollars Without Any Proof Of Income

Types of Student Loans

Understanding the different types of student loans is essential when exploring repayment and forgiveness options. Here are the main types of student loans you may encounter:

Subsidized Loans

Subsidized loans are a type of federal loan available to undergraduate students with demonstrated financial need. The government covers the cost of interest while you are in school, during periods of deferment, and for the first six months after you graduate or leave school.

Unsubsidized Loans

Unsubsidized loans are also federal loans but are not based on financial need. Unlike subsidized loans, interest begins accruing on unsubsidized loans as soon as the loan is disbursed.

Perkins Loans

Perkins loans are low-interest federal loans available to students with exceptional financial need. These loans are administered by your school and are subject to the school’s terms and conditions.

Direct Loans

Direct loans are federal loans issued to students and parents. These loans are funded by the U.S. Department of Education and are available to both undergraduate and graduate students. Direct loans include Direct Subsidized Loans, Direct Unsubsidized Loans, and Direct PLUS Loans.

Federal Family Education Loan

Federal Family Education Loan (FFEL) Program loans are federal loans made by private lenders and guaranteed by the federal government. While no new loans are being made under this program, some borrowers may still have existing FFEL Program loans.

Loan Forgiveness and Tax Implications

It is important to understand the potential tax implications of receiving loan forgiveness. While loan forgiveness can provide significant relief from your student debt, it may be considered taxable income by the IRS. Any amount forgiven may be subject to income tax unless you qualify for an exclusion or exception.

Tax Implications of Loan Forgiveness

In general, loan forgiveness is considered taxable income by the IRS. However, there are certain exceptions and exclusions that may apply. For example, if you qualify for Public Service Loan Forgiveness or Teacher Loan Forgiveness, the forgiven amount may not be subject to income tax. It is crucial to consult a tax professional or refer to the IRS guidelines to understand the tax implications of your specific loan forgiveness situation.

Loan Forgiveness in CARES Act

Due to the COVID-19 pandemic, the CARES Act was passed to provide relief to borrowers with federal student loans. Under the CARES Act, all interest and principal payments on federally held loans were automatically suspended until September 30, 2021, providing temporary relief from loan payments. Additionally, any payments made during this period were treated as qualifying payments for loan forgiveness programs, such as Public Service Loan Forgiveness.

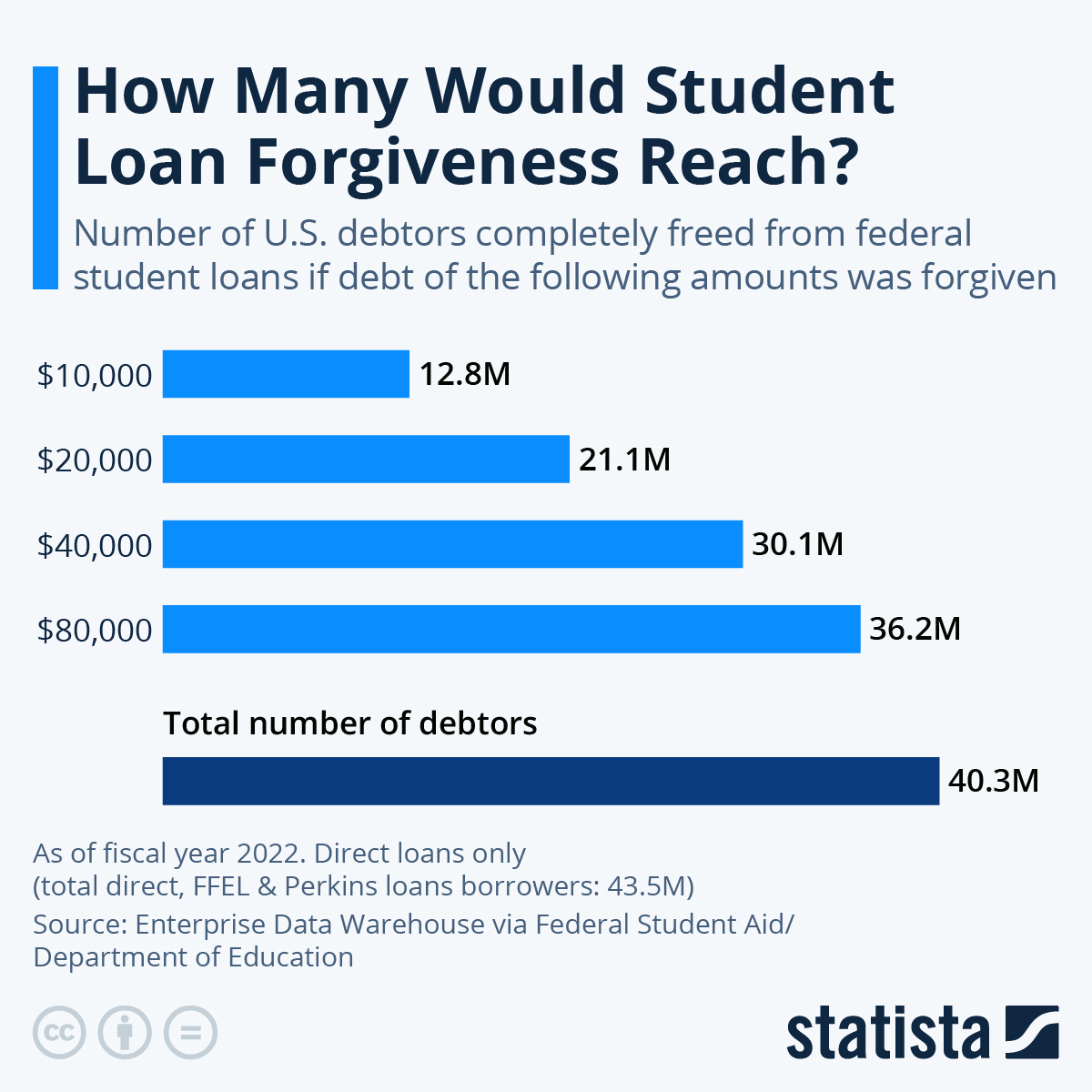

This image is property of cdn.statcdn.com.

How To Access Up To One Million Dollars Without Any Proof Of Income

Application Process

The application process for loan forgiveness or other repayment options may vary depending on the program or option you choose. Generally, you will need to gather the necessary documentation, complete an application, and submit it to the appropriate authority or loan servicer. It is important to follow the specific filing procedures outlined by each program and ensure that you provide accurate and up-to-date information.

Filing Procedures

Each loan forgiveness program or option may have specific filing procedures and requirements. For federal loan forgiveness programs, you will typically need to submit an application to the U.S. Department of Education or your loan servicer. Additionally, you may need to provide supporting documentation, such as proof of employment or income. Private loan forgiveness options may have different filing procedures, and it is important to contact your loan servicer directly for guidance on the application process.

Documentation Required

When applying for loan forgiveness or other repayment options, you will likely need to provide supporting documentation to verify your eligibility. Common documentation requirements may include tax returns, pay stubs, employment certification, proof of enrollment in a qualifying program, or proof of disability. It is important to gather and submit all required documentation accurately and within the specified timeline to ensure your application is processed efficiently.

Loan Default and Repayment Assistance

Loan default occurs when you fail to make payments on your student loans as scheduled. Defaulting on your loans can have serious consequences, including damage to your credit score, wage garnishment, and potential legal action. However, there are repayment assistance options available to help you avoid default and manage your student loan debt effectively.

Consequences of Loan Default

Defaulting on your student loans can have long-lasting consequences. Your loan servicer may report your default to credit bureaus, resulting in a negative impact on your credit score. A lower credit score can make it difficult to qualify for future loans or credit cards and may even affect your ability to rent an apartment or secure employment. In addition, your loan servicer or the government may take legal action to collect the debt, which can result in wage garnishment or other financial penalties.

Loan Rehabilitation Options

Loan rehabilitation is a way to get out of default and bring your loans back into good standing. By entering into a loan rehabilitation program, you can set up an affordable payment plan based on your income and family size. Making the agreed-upon payments for a certain period of time, typically nine months, can help you rehabilitate your loans and remove the default status from your credit report.

Loan Discharge Due to Default

In certain cases, you may be eligible for loan discharge due to default. Loan discharge due to default is typically available in cases of fraud, school closure, or false certification. If you believe you qualify for loan discharge due to default, it is important to contact your loan servicer or the U.S. Department of Education to understand the specific requirements and application process.

In conclusion, managing student loan debt can be challenging, but there are options available to help you alleviate the burden. Whether through loan forgiveness programs, income-driven repayment options, or debt relief programs, it is essential to explore the various avenues and understand the eligibility criteria and application processes. By taking the necessary steps and being proactive in managing your student loans, you can work towards financial freedom and ultimately achieve your educational and career goals.

How To Access Up To One Million Dollars Without Any Proof Of Income