If you’re a parent looking to finance your child’s college education, it’s important to understand Parent PLUS Loans. These loans, offered by the U.S. Department of Education, can help cover the costs of tuition, room and board, and other expenses. With their flexible repayment options and low interest rates, Parent PLUS Loans are a popular choice for many families. In this article, we will explore the ins and outs of these loans, making sure you have all the information you need to make an informed decision about financing your child’s education.

What are Parent PLUS Loans?

Definition and purpose

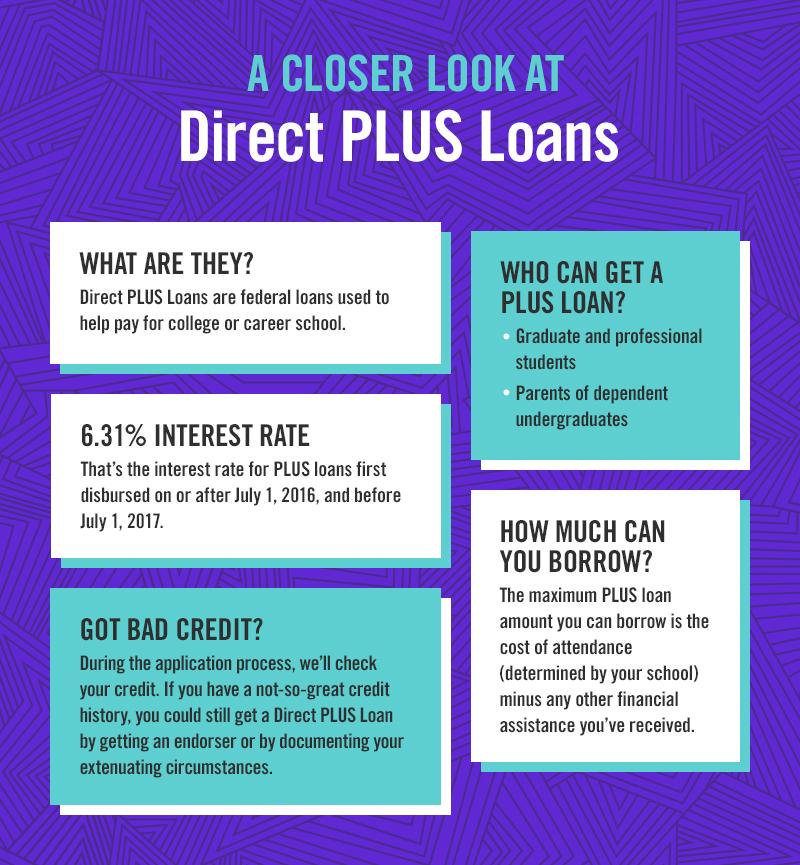

Parent PLUS Loans are federal loans that parents can take out to help pay for their child’s college education. These loans are offered by the U.S. Department of Education and are designed to supplement other forms of financial aid, such as grants, scholarships, and student loans. Parent PLUS Loans have a fixed interest rate, making them a predictable and reliable source of funds for families who are unable to cover the full cost of tuition and other expenses.

Eligibility criteria

To be eligible for Parent PLUS Loans, you must be the parent (biological, adoptive, or in some cases, stepparent) of a dependent undergraduate student who is enrolled at least half-time in an eligible program at an accredited institution. You must also meet certain credit requirements, including not having an adverse credit history. The student must also meet all federal student aid eligibility requirements.

Loan limits

The amount you can borrow through Parent PLUS Loans is determined by the cost of attendance at your child’s college or university, minus any other financial aid they receive. There is no strict limit on the maximum amount you can borrow, but there is a cap on the loan amount based on your creditworthiness. It’s important to note that Parent PLUS Loans are not need-based, so you can borrow the full cost of attendance regardless of your financial situation.

How does Parent PLUS Loans work?

Application process

To apply for a Parent PLUS Loan, you must first complete the Free Application for Federal Student Aid (FAFSA) for the academic year in which you need the loan. Once you’ve completed the FAFSA, you can then apply for the Parent PLUS Loan online through the U.S. Department of Education’s website or by completing a paper application. You will need to provide your personal and financial information, as well as the school’s information and the loan amount you wish to borrow.

Loan disbursement

Once your application for a Parent PLUS Loan is approved, the funds will be disbursed directly to your child’s college or university. Typically, the school will first apply the funds to tuition and fees, and any remaining amount will be refunded to either you or your child, depending on the school’s policy. It’s important to note that Parent PLUS Loans are disbursed in multiple installments, typically once per semester or trimester.

Repayment options

Repayment of Parent PLUS Loans typically begins within 60 days after the loan is fully disbursed. However, you have the option to request a deferment while your child is enrolled at least half-time, which allows you to postpone making payments until after they graduate or drop below half-time enrollment. Parent PLUS Loans offer several repayment options, including a standard repayment plan with fixed monthly payments over 10 years, a graduated repayment plan with lower initial payments that increase over time, and an income-contingent repayment plan that adjusts your monthly payments based on your income and family size.

This image is property of www.edvisors.com.

Benefits of Parent PLUS Loans

Access to higher education

One of the main benefits of Parent PLUS Loans is that they provide families with the financial means to afford higher education for their children. Without these loans, many students would be unable to attend college or would have to rely on alternative, often more expensive forms of financing such as private loans. Parent PLUS Loans ensure that qualified students have access to the education they need to pursue their career goals.

Flexible repayment options

Parent PLUS Loans offer flexibility when it comes to repayment. The standard repayment plan allows you to pay off the loan over a fixed period of time, while the graduated repayment plan starts with lower payments that increase every two years. This can be helpful if you anticipate your income increasing in the future. The income-contingent repayment plan adjusts your monthly payments based on your income, making it more manageable if your income is currently lower or if you have other financial obligations.

Fixed interest rates

Parent PLUS Loans have a fixed interest rate, meaning that the rate remains the same throughout the life of the loan. This provides a level of predictability and stability, as you will always know exactly how much interest you will be paying. Fixed interest rates can be advantageous when compared to variable interest rates, which can fluctuate over time and potentially increase your monthly payments.

Considerations before applying for Parent PLUS Loans

Financial implications

Before applying for Parent PLUS Loans, it’s important to carefully consider the financial implications. These loans can add to your overall debt burden, and it’s crucial to assess whether you have the ability to repay them while still meeting your other financial obligations. Consider your current income, expenses, and future financial goals to determine if taking on this additional debt is the right decision for your family.

Impact on credit score

Applying for a Parent PLUS Loan will involve a credit check, and if approved, the loan will be listed on your credit report. It’s important to understand that taking on this debt could have an impact on your credit score, particularly if you have a large amount of existing debt or if you miss any loan payments. It’s crucial to make timely payments and manage your debt responsibly to maintain a good credit score.

Other available financial aid options

Before deciding to take out a Parent PLUS Loan, explore other available financial aid options. Your child may qualify for grants, scholarships, or work-study programs that can help offset the cost of education. Additionally, your child may be eligible for federal student loans with lower interest rates and more favorable repayment terms. Consider all of these options before making a final decision on whether to pursue a Parent PLUS Loan.

This image is property of www.cfnc.org.

Understanding the interest rates of Parent PLUS Loans

How interest rates are determined

The interest rate for Parent PLUS Loans is determined each year by the U.S. Department of Education. The rate is based on the 10-year Treasury note auction rate, with an additional percentage added to cover administrative costs. The resulting interest rate is fixed for the life of the loan. The exact interest rate you receive will depend on the year in which you borrow the loan.

Current interest rates

As of the 2021-2022 academic year, the interest rate for Parent PLUS Loans is 6.28%. It’s important to note that this rate can change annually, so it’s crucial to check the most up-to-date information on the U.S. Department of Education’s website or speak with your loan servicer for accurate information about the current interest rates.

Interest rate caps

Parent PLUS Loans do have an interest rate cap, which means that there is a maximum interest rate that can be charged on the loan. This cap provides borrowers with some protection against excessive interest rates. However, it’s important to note that the interest rates for Parent PLUS Loans tend to be higher than those for other types of federal student loans, so it’s crucial to carefully consider the long-term cost of borrowing before committing to a Parent PLUS Loan.

Repayment options for Parent PLUS Loans

Standard repayment plan

The standard repayment plan for Parent PLUS Loans has fixed monthly payments over a period of 10 years. This plan allows you to pay off the loan in a shorter amount of time, but monthly payments may be higher compared to other repayment options. If you can afford the higher payments and want to pay off the loan as quickly as possible, the standard repayment plan may be the right choice for you.

Graduated repayment plan

The graduated repayment plan for Parent PLUS Loans starts with lower monthly payments that increase every two years. This plan is suitable for borrowers who anticipate their income increasing over time or who want to start with lower payments early on. Keep in mind that although the monthly payments will start lower, the overall cost of the loan may be higher due to accruing interest.

Income-contingent repayment plan

The income-contingent repayment plan for Parent PLUS Loans adjusts your monthly payments based on your income and family size. This plan can be beneficial if your income is currently lower or if you have other financial obligations. Your payments will be recalculated each year based on your current income and financial situation. It’s important to note that under this plan, you may end up paying more in interest over the life of the loan compared to the standard or graduated repayment plans.

This image is property of leveredge-application-public.s3.amazonaws.com.

Tips for managing Parent PLUS Loans

Create a budget

To effectively manage your Parent PLUS Loans, create a budget that includes your loan payments as part of your monthly expenses. This will help you allocate funds appropriately and ensure that you have enough money to make your loan payments on time. A budget can also help you identify areas where you can cut back on spending and save money, allowing you to put more towards your loan payments.

Explore loan forgiveness programs

Depending on your profession and financial circumstances, you may be eligible for loan forgiveness programs that could significantly reduce or eliminate your Parent PLUS Loan balance. For example, some teachers, nurses, or public service employees may qualify for loan forgiveness after a certain number of years of service. It’s important to research and understand the eligibility requirements for these programs and consider if they align with your career goals.

Communicate with the loan servicer

If you encounter any difficulties or changes in your financial situation that make it challenging to make your loan payments, it’s important to communicate with your loan servicer. They may be able to offer alternative repayment options or assistance programs to help you through difficult times. Ignoring the issue or defaulting on your loans will only worsen the situation, so it’s crucial to be proactive and reach out to your loan servicer for guidance and support.

Possible consequences of defaulting on Parent PLUS Loans

Damage to credit score

Defaulting on your Parent PLUS Loans can have severe consequences for your credit score. Missed or late payments will be reported to credit bureaus and can significantly lower your credit score, making it more difficult to secure favorable interest rates for future loans or qualify for other types of credit, such as mortgages or car loans. It’s crucial to make your loan payments on time to protect your creditworthiness.

Garnishment of wages

If you default on your Parent PLUS Loans, the U.S. Department of Education has the authority to garnish your wages. This means that a portion of your paycheck will be automatically withheld to repay your loan. Wage garnishment can make it even more difficult to manage your finances and meet your other financial obligations. It’s important to understand the potential consequences of defaulting and to take steps to prevent it from happening.

Loss of eligibility for future financial aid

Defaulting on your Parent PLUS Loans can also result in the loss of eligibility for future financial aid, both for yourself and potentially for your child. This can make it even more challenging to afford higher education for your family members in the future. To avoid this loss of eligibility, it’s crucial to stay on top of your loan payments and communicate with your loan servicer if you’re facing financial difficulties.

This image is property of s28637.pcdn.co.

Alternatives to Parent PLUS Loans

Federal student loans

Before considering Parent PLUS Loans, it’s worth exploring other federal student loan options. Direct Subsidized Loans and Direct Unsubsidized Loans are available to undergraduate students and come with lower interest rates and more favorable repayment terms compared to Parent PLUS Loans. Your child may be eligible for these loans depending on their financial need and other factors.

Private student loans

Private student loans are another alternative to Parent PLUS Loans. These loans are offered by private lenders and typically have higher interest rates and stricter repayment terms compared to federal student loans. However, if you have a strong credit history or are willing to use a co-signer with good credit, private student loans may be an option worth considering.

Scholarships and grants

Scholarships and grants are forms of financial aid that do not have to be repaid. They are typically awarded based on academic or athletic achievements, financial need, or other criteria. Encourage your child to actively search for scholarships and grants that they may be eligible for, as these can significantly reduce the need for loans and make college more affordable.

Conclusion

Parent PLUS Loans can be a valuable resource for families who need additional financial assistance to cover the cost of their child’s college education. These loans provide access to higher education, offer flexible repayment options, and come with fixed interest rates. However, it’s important to carefully consider the financial implications and explore all available options before committing to Parent PLUS Loans. By understanding the loan terms, managing your finances responsibly, and seeking assistance when needed, you can navigate the repayment process successfully and provide your child with the education they deserve.

This image is property of pbs.twimg.com.