Looking to refinance your home equity loan? Home equity loan refinancing allows you to take advantage of lower interest rates, potentially saving you money on your monthly payments. This process involves replacing your existing loan with a new one, using the equity in your home as collateral. Whether you’re looking to consolidate debt, make home improvements, or simply lower your interest rate, home equity loan refinancing can be a beneficial financial move. In this article, we’ll explore the key terms and concepts related to home equity loan refinancing, providing you with the knowledge you need to make informed decisions about your financial future.

How To Access Up To One Million Dollars Without Any Proof Of Income

What is Home Equity Loan Refinancing?

Home equity loan refinancing is a process that allows you to replace your current home equity loan with a new loan, often with better terms and lower interest rates. It involves getting a new loan to pay off your existing loan and using the equity in your home as collateral.

Definition of home equity loan refinancing

Home equity loan refinancing refers to the process of replacing your current home equity loan with a new loan that has different terms, interest rates, and repayment options. By refinancing, you can take advantage of lower interest rates, access cash for major expenses, consolidate debt, and change loan terms.

How it works

Home equity loan refinancing works by applying for a new loan with a lender and using the funds from that loan to pay off your current home equity loan. The new loan will have different terms, such as interest rates and repayment options, which can potentially save you money over the long term. The equity in your home is used as collateral for the new loan.

Benefits of home equity loan refinancing

There are several benefits to home equity loan refinancing:

-

Lower interest rates: Refinancing can help you take advantage of lower interest rates, which can save you money on your monthly payments and overall interest costs.

-

Improving credit score: By refinancing and making timely payments on your new loan, you can improve your credit score over time. This can open up opportunities for better loan terms and lower interest rates in the future.

-

Consolidating debt: Refinancing allows you to consolidate multiple debts into one loan, simplifying your finances and potentially reducing your overall monthly payments.

-

Accessing cash for major expenses: Refinancing can provide you with access to cash for major expenses, such as home renovations, education costs, or medical bills.

-

Changing loan terms: Refinancing gives you the opportunity to change the terms of your loan, such as extending the repayment period or switching from an adjustable-rate mortgage to a fixed-rate mortgage.

When Should You Consider Home Equity Loan Refinancing?

There are several situations where you should consider home equity loan refinancing:

Lower interest rates

If interest rates have decreased since you took out your current home equity loan, it may be a good time to consider refinancing. By getting a new loan with a lower interest rate, you can save money on your monthly payments and overall interest costs.

Improving credit score

If your credit score has improved since you took out your current home equity loan, you may be eligible for better loan terms and lower interest rates through refinancing. This can save you money over the long term and improve your overall financial situation.

Consolidating debt

If you have multiple debts, such as credit card debt or other loans, refinancing your home equity loan can help you consolidate all your debts into one loan with a potentially lower interest rate. This can simplify your finances and reduce your overall monthly payments.

Accessing cash for major expenses

If you need cash for major expenses, such as home renovations, education costs, or medical bills, refinancing your home equity loan can provide you with the funds you need. By tapping into the equity in your home, you can access cash at a potentially lower interest rate than other forms of borrowing.

Changing loan terms

If you want to change the terms of your loan, such as extending the repayment period or switching from an adjustable-rate mortgage to a fixed-rate mortgage, refinancing can help you achieve these goals. It allows you to customize your loan to fit your current financial needs and long-term goals.

How To Access Up To One Million Dollars Without Any Proof Of Income

Factors to Consider Before Refinancing

Before refinancing your home equity loan, there are several factors you should consider:

Current interest rates

One of the most important factors to consider before refinancing is the current interest rates. If interest rates have decreased since you took out your current loan, it may be a good time to refinance and take advantage of the lower rates. However, if interest rates have increased, refinancing may not be the best option for you.

Equity in your home

The amount of equity you have in your home is another important factor to consider before refinancing. Lenders typically require a certain amount of equity in your home to approve a refinancing application. If you have a significant amount of equity, you may be eligible for better loan terms and lower interest rates.

Credit score

Your credit score plays a crucial role in the refinancing process. Lenders use your credit score to determine your creditworthiness and the interest rates you qualify for. Before refinancing, it’s important to review your credit score and work on improving it if needed. A higher credit score can help you qualify for better loan terms and lower interest rates.

Debt-to-income ratio

Your debt-to-income ratio is another factor that lenders consider when reviewing your refinancing application. It measures the amount of your monthly income that goes towards paying off debts. Lenders typically have a maximum debt-to-income ratio they are willing to accept. It’s important to calculate your debt-to-income ratio before applying for refinancing to ensure you meet the lender’s requirements.

Loan-to-value ratio

The loan-to-value ratio is the ratio of the loan amount to the appraised value of your home. Lenders use this ratio to assess the risk of lending to you. A lower loan-to-value ratio indicates less risk for the lender. It’s important to calculate your loan-to-value ratio before refinancing to determine if you have enough equity in your home to meet the lender’s requirements.

The Refinancing Process

The refinancing process can be broken down into several steps:

Researching lenders

The first step in the refinancing process is to research different lenders and compare their offers. Look for lenders that specialize in home equity loan refinancing and have competitive interest rates and fees. Reading reviews and getting recommendations from friends or family members can also be helpful in finding the right lender for your needs.

Gathering necessary documentation

Once you’ve chosen a lender, you’ll need to gather the necessary documentation for the refinancing application. This typically includes proof of income, such as pay stubs or tax returns, bank statements, and documentation of your current home equity loan.

Submitting the application

After gathering all the necessary documentation, you can submit your refinancing application to the lender. The lender will review your application and documentation to assess your eligibility for refinancing. This process may take some time, so it’s important to be patient.

Loan approval and underwriting

If your application is approved, the lender will move forward with the underwriting process. This involves verifying the information you provided in the application and assessing the risk of lending to you. The lender may request additional documentation or ask for clarification on certain information.

Home appraisal

As part of the refinancing process, the lender will typically require a home appraisal to determine the current value of your property. This is done to ensure that the loan amount does not exceed the appraised value of the home. The appraisal is conducted by a certified appraiser and may require an inspection of the property.

Closing costs and fees

Before finalizing the refinancing, you’ll need to pay the closing costs and fees associated with the loan. These costs can include origination fees, appraisal fees, credit report fees, and attorney fees, among others. It’s important to review the closing costs and fees before proceeding with the refinancing to ensure you understand the total cost of the loan.

Signing the loan agreement

Once all the necessary steps have been completed, you will sign the loan agreement to finalize the refinancing. This legally binds you to the terms and conditions of the new loan. It’s important to review the loan agreement carefully and seek professional advice if needed before signing.

How To Access Up To One Million Dollars Without Any Proof Of Income

Types of Home Equity Loan Refinancing

There are several types of home equity loan refinancing options to choose from:

Traditional home equity loan refinancing

This type of refinancing involves getting a new loan with a fixed interest rate and a fixed repayment period. It allows you to replace your current home equity loan with a new loan that has better terms and potentially lower interest rates.

Home equity line of credit (HELOC)

A home equity line of credit (HELOC) is a line of credit that is secured by your home’s equity. It works like a credit card, where you can borrow funds as needed, up to a certain credit limit. A HELOC offers flexibility in accessing funds and typically has a variable interest rate.

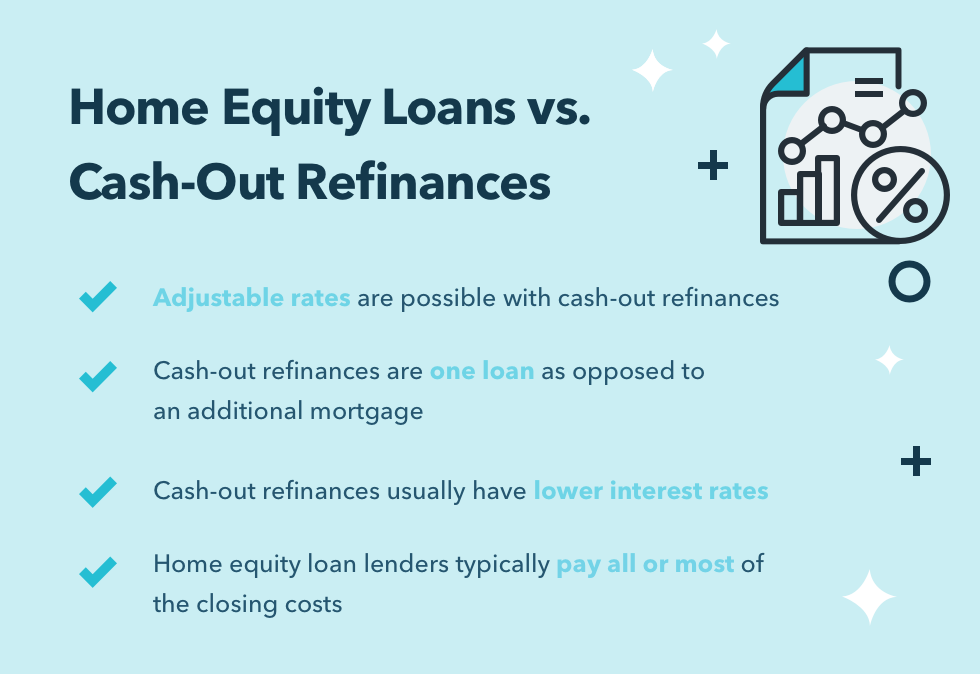

Cash-out refinance

A cash-out refinance allows you to borrow more than the amount needed to pay off your current home equity loan. The additional funds can be used for various purposes, such as home renovations, debt consolidation, or other major expenses. A cash-out refinance can provide you with access to cash while potentially improving your loan terms.

Advantages of Home Equity Loan Refinancing

Home equity loan refinancing offers several advantages:

Lower interest rates

One of the main advantages of refinancing is the opportunity to secure a lower interest rate. Lower interest rates can save you money on your monthly payments and overall interest costs over the life of the loan.

Lower monthly payments

By refinancing, you may be able to lower your monthly mortgage payments. This can provide you with additional cash flow and make it easier to manage your monthly budget.

Consolidation of debt

Refinancing allows you to consolidate multiple debts, such as credit card debt or other loans, into one loan. This can simplify your finances and potentially reduce your overall monthly payments.

Access to cash

Refinancing can provide you with access to cash for major expenses, such as home renovations, education costs, or medical bills. By tapping into the equity in your home, you can access funds at a potentially lower interest rate than other forms of borrowing.

Flexible loan terms

Refinancing gives you the opportunity to change the terms of your loan to fit your current financial needs and long-term goals. You can adjust the repayment period, switch from an adjustable-rate mortgage to a fixed-rate mortgage, or customize the loan to meet your specific requirements.

How To Access Up To One Million Dollars Without Any Proof Of Income

Disadvantages of Home Equity Loan Refinancing

While home equity loan refinancing has its advantages, there are also some disadvantages to consider:

Additional fees and closing costs

Refinancing involves additional fees and closing costs, such as origination fees, appraisal fees, and attorney fees. These costs can add up and increase the overall cost of the loan. It’s important to carefully review the fees and closing costs before proceeding with the refinancing.

Risk of foreclosure

When you refinance your home equity loan, you’re taking on a new loan that uses your home as collateral. If you’re unable to make the payments on the new loan, there is a risk of foreclosure. It’s important to carefully consider your ability to make the payments before refinancing.

Long-term debt

Refinancing extends the term of your loan, which means you’ll be paying off your debt over a longer period of time. While this can lower your monthly payments, it also means you’ll be in debt for a longer period.

Potential impact on credit score

Refinancing can have an impact on your credit score. When you apply for a new loan, the lender will perform a hard inquiry on your credit report, which can temporarily lower your credit score. Additionally, if you’re unable to make the payments on the new loan, it can have a negative impact on your credit score.

Tips for Getting the Best Refinancing Deal

Here are some tips for getting the best refinancing deal:

Comparison shopping for lenders

Take the time to shop around and compare offers from different lenders. Look for lenders that specialize in home equity loan refinancing and have competitive interest rates and fees. This will help you find the best deal that suits your needs.

Improving credit score before applying

Before applying for refinancing, it’s a good idea to review your credit score and work on improving it if needed. A higher credit score can help you qualify for better loan terms and lower interest rates.

Negotiating for lower interest rates and fees

Don’t be afraid to negotiate with lenders for lower interest rates and fees. If you have a good credit score and a strong financial profile, you may be able to secure better terms by negotiating.

Calculating the break-even point

Before refinancing, calculate the break-even point, which is the point at which the savings from refinancing outweigh the costs. This will help you determine if refinancing is financially beneficial for you.

Avoiding predatory lending practices

Be cautious of predatory lending practices, such as lenders who pressure you into refinancing or offer terms that seem too good to be true. Always read the fine print and understand the terms and conditions of the loan before signing anything.

How To Access Up To One Million Dollars Without Any Proof Of Income

Alternatives to Home Equity Loan Refinancing

If home equity loan refinancing is not the right option for you, there are several alternatives to consider:

Personal loan

A personal loan is an unsecured loan that can be used for various purposes, such as debt consolidation or major expenses. Personal loans typically have higher interest rates than home equity loans, but they don’t require collateral.

Credit card balance transfer

If you have credit card debt, you may be able to transfer the balance to a credit card with a lower interest rate. This can help you save money on interest charges and potentially pay off the debt faster.

Second mortgage

A second mortgage is a loan that uses the equity in your home as collateral. It allows you to borrow against the equity in your home while keeping your original mortgage intact.

Loan modification

If you’re struggling to make your current mortgage payments, you may be able to work with your lender to modify the loan terms. A loan modification can help lower your monthly payments and make them more affordable.

FAQs About Home Equity Loan Refinancing

How long does the refinancing process take?

The refinancing process can take anywhere from 30 to 45 days, depending on various factors such as the lender’s processes and the complexity of your application.

Can I refinance with bad credit?

While it may be more challenging to refinance with bad credit, it is still possible. Lenders may have specific requirements and higher interest rates for borrowers with bad credit.

What are the closing costs for refinancing?

Closing costs for refinancing can vary depending on the lender and the specifics of your loan. Typical closing costs include appraisal fees, origination fees, title search fees, and attorney fees.

Will refinancing affect my credit score?

Refinancing can temporarily lower your credit score due to the hard inquiry on your credit report. However, if you make timely payments on the new loan, it can have a positive impact on your credit score over time.

Can I refinance if I have an underwater mortgage?

If you have an underwater mortgage, where you owe more on your home than its current value, it may be challenging to refinance. However, certain government programs, such as the FHA Streamline Refinance, can help underwater homeowners refinance their loans. It’s best to consult with a lender or mortgage professional to explore your options.

How To Access Up To One Million Dollars Without Any Proof Of Income