Looking to refinance your home equity loan? It’s a smart move that can help you save money and achieve your financial goals. Refinancing allows you to replace your current loan with a new one, often at a lower interest rate. By doing so, you can reduce your monthly payments and potentially pay off your debt faster. With terms like refinancing, interest rate, equity, and mortgage, it may seem overwhelming, but don’t worry! In this article, we’ll break down the essentials of refinancing a home equity loan, explain key terms, and provide you with the information you need to make an informed decision. So, let’s get started on your path to financial freedom!

How To Access Up To One Million Dollars Without Any Proof Of Income

What is a Home Equity Loan?

A home equity loan is a type of loan that allows you to borrow money against the equity you have built up in your home. Equity is the difference between the appraised value of your home and the amount you still owe on your mortgage. With a home equity loan, homeowners are able to access funds for various purposes, such as home improvements, debt consolidation, or paying for college tuition.

Definition of a home equity loan

A home equity loan, also known as a second mortgage, is a loan that uses your home as collateral. It allows you to borrow a lump sum of money and repay it over time with fixed monthly payments. The loan is typically structured with a fixed interest rate and term, making it easier to budget for and manage.

How it differs from other types of loans

What sets a home equity loan apart from other types of loans is the collateral involved. When you take out a personal loan or credit card, there is no collateral tied to the loan. This means that if you default on the loan, the lender has no specific asset to reclaim. In contrast, a home equity loan is secured by your home, which gives the lender the right to repossess your property if you fail to make the required payments.

How it works

To obtain a home equity loan, you must have equity in your home. The amount of equity you can borrow against depends on the appraised value of your home and the loan-to-value ratio established by the lender. Once approved, you will receive a lump sum of money. You then make regular monthly payments, including principal and interest, over the agreed-upon term until the loan is fully repaid.

Reasons to Refinance a Home Equity Loan

Refinancing a home equity loan can provide borrowers with several potential advantages. Here are some common reasons why homeowners choose to refinance their home equity loans:

Lower interest rates

One of the main reasons homeowners choose to refinance their home equity loans is to take advantage of lower interest rates. If market rates have dropped since you obtained your original loan, refinancing can allow you to secure a new loan with a lower interest rate. This can save you money on interest payments over the life of the loan.

Cash-out refinancing

Another reason to refinance a home equity loan is to access cash. With cash-out refinancing, homeowners can borrow more than their outstanding loan balance and receive the difference in cash. This can be useful for major expenses such as home renovations, paying off high-interest debt, or funding an education.

Changing loan terms

Refinancing also gives homeowners the opportunity to change the terms of their loan. For example, if you have a variable-rate loan and want to switch to a fixed-rate loan for more stability, refinancing can make that possible. Additionally, you may be able to extend or shorten the term of your loan.

Debt consolidation

Those with high-interest debt may choose to refinance their home equity loan as a way to consolidate their debt. By combining multiple loans into one, you can simplify your financial obligations and potentially secure a lower interest rate, reducing the overall cost of your debt.

Repairs and renovations

If you’re planning on making significant repairs or renovations to your home, refinancing your home equity loan could provide the necessary funds. By refinancing, you can tap into your home’s equity and use the money to cover the costs of these projects.

How To Access Up To One Million Dollars Without Any Proof Of Income

Preparing to Refinance

Before proceeding with refinancing your home equity loan, there are a few steps you should take to ensure a smooth process:

Review your credit score

Your credit score plays a significant role in the approval process and the interest rate you will be offered. Take the time to review your credit score and address any issues before applying to refinance. Pay off outstanding debts, resolve any errors on your credit report, and demonstrate responsible credit management.

Assess your home equity

It’s essential to determine how much equity you have in your home before refinancing. Lenders typically have a maximum loan-to-value ratio that they will lend against. Calculate your home’s appraised value and subtract the remaining balance on your mortgage to determine your available equity.

Calculate your debt-to-income ratio

Lenders will evaluate your debt-to-income ratio when considering your refinancing application. Calculate this ratio by dividing your total monthly debt payments by your monthly income. Aim for a debt-to-income ratio below 43% to increase your chances of approval.

Research potential lenders

Take the time to research different lenders and read reviews to find a reputable institution to work with. Compare interest rates, terms, and fees to ensure you’re making an informed decision.

Gather necessary documents

Before applying to refinance, gather the necessary documents to support your application. This may include recent tax returns, pay stubs, bank statements, and documentation related to your existing home equity loan.

The Refinancing Process

Once you have completed the necessary preparations, you can begin the refinancing process. Here is an overview of the steps involved:

Submitting an application

The refinancing process begins with completing and submitting an application. Provide accurate and up-to-date information about your income, assets, and property. Be prepared to disclose your credit history and any outstanding debts.

Loan underwriting

After submitting your application, the lender will review your information and verify the details provided. This process is known as underwriting. The lender will assess your creditworthiness, income, and the value of your home to determine if you qualify for refinancing.

Home appraisal

As part of the underwriting process, the lender will require a home appraisal. A professional appraiser will assess the current market value of your home to ensure that the loan amount aligns with the property’s worth.

Credit report check

The lender will also review your credit report to assess your creditworthiness. They will consider factors such as your payment history, outstanding debts, and credit utilization. A good credit score can increase your chances of approval and secure better refinancing terms.

Loan approval or denial

Once the underwriting process is complete, the lender will notify you of their decision. If approved, you will receive loan details outlining the terms, interest rate, and monthly payments. If denied, the lender will provide an explanation for the decision.

How To Access Up To One Million Dollars Without Any Proof Of Income

Understanding Refinancing Options

When refinancing your home equity loan, there are various options available. Familiarize yourself with the following choices to make an informed decision:

Fixed-rate refinancing

A fixed-rate refinancing option allows borrowers to lock in an interest rate for the duration of the loan term. This provides stability as your monthly payments remain the same, regardless of fluctuations in the market.

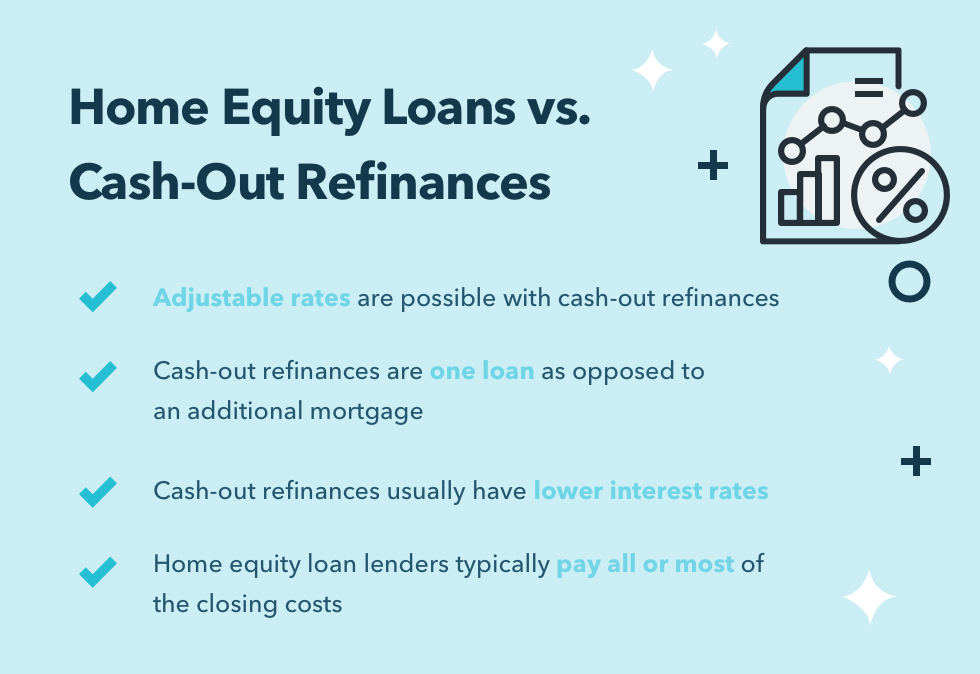

Adjustable-rate refinancing

With an adjustable-rate refinancing option, the interest rate is variable and can change over time. This means that your monthly payments may increase or decrease based on market conditions. Adjustable-rate loans often start with a fixed rate for an initial period before transitioning to a variable rate.

FHA refinancing

The Federal Housing Administration (FHA) offers refinancing options for borrowers who may not meet conventional lending criteria. FHA loans typically require a lower down payment and have more flexible credit requirements.

Cash-out refinancing

Cash-out refinancing allows homeowners to borrow more than the outstanding loan balance and receive the difference in cash. This option is beneficial for those looking to access funds for large expenses, such as home renovations or consolidating debt.

Rate lock options

Some lenders offer rate lock options, which allow borrowers to secure a specific interest rate for a defined period. Rate locks can protect borrowers from potential rate increases during the refinancing process.

Benefits and Drawbacks of Refinancing a Home Equity Loan

Before proceeding with refinancing, it’s essential to consider the potential benefits and drawbacks. Here are some factors to keep in mind:

Lower monthly payments

Refinancing a home equity loan may result in lower monthly payments. By securing a lower interest rate or extending the loan term, you can reduce the amount owed each month, freeing up funds for other expenses.

Interest rate reduction

Refinancing can lead to a reduction in the interest rate on your loan. This can save you a significant amount of money over the life of the loan, especially if market interest rates have dropped since you obtained your original loan.

Consolidating debt

Refinancing provides an opportunity to consolidate high-interest debt into one loan with a lower interest rate. This can simplify your financial obligations and potentially save you money on interest payments.

Accessing cash

Cash-out refinancing allows homeowners to access the equity in their homes and receive the difference in cash. This can be useful for funding large expenses or investments.

Extended loan term

While extending the loan term can lower your monthly payments, it may increase the overall cost of the loan. Consider the long-term financial implications and decide if the trade-off is worthwhile.

Closing costs and fees

Refinancing typically involves closing costs and fees, just like obtaining an initial mortgage. It’s important to consider these additional costs and factor them into your decision-making process.

How To Access Up To One Million Dollars Without Any Proof Of Income

Calculating the Costs of Refinancing

When refinancing a home equity loan, it’s crucial to be aware of the costs involved. Here are some common expenses to consider:

Origination fees

Origination fees are charged by lenders to cover the cost of processing the loan. They typically range from 1% to 3% of the loan amount.

Appraisal fees

An appraisal fee is incurred when a professional appraiser assesses the current market value of your home. The fee covers the cost of their services and can range from a few hundred to several thousand dollars.

Title search and insurance

To ensure clear ownership of the property, lenders often require a title search and insurance. These costs cover the examination of public records and protect against any legal issues with the title.

Loan officer fees

Loan officers may charge fees for their services, including reviewing and processing your application. These fees can vary depending on the lender and the complexity of your refinancing.

Prepayment penalties

Some home equity loans may include prepayment penalties. These fees are charged if you pay off the loan early or refinance within a certain period. Review your loan terms to determine if any prepayment penalties apply.

Potential Risks and Considerations

While refinancing a home equity loan can provide benefits, it’s crucial to be aware of potential risks and considerations. Here are some factors to keep in mind:

Potential loss of home equity

Refinancing your home equity loan may result in a loss of equity if you take out more than the outstanding loan balance. This can impact your overall net worth and the amount of money you can access in the future.

Impact on credit score

Refinancing can temporarily lower your credit score due to the credit checks and inquiries involved in the process. However, if you consistently make your payments on time, your credit score is likely to improve over time.

Long-term financial implications

Extending the loan term during refinancing can result in more interest paid over the life of the loan. Consider the overall cost and if the potential benefits outweigh the long-term financial implications.

Refinancing fees and expenses

Refinancing involves various fees and expenses, which can add to the overall cost. Take into account these costs and determine if the potential savings outweigh them.

Balloon payments

Some refinancing options may include balloon payments, where a large sum is due at the end of the loan term. Be sure to fully understand the terms of the loan and how it will impact your financial situation.

How To Access Up To One Million Dollars Without Any Proof Of Income

Tips for a Successful Refinancing

To ensure a successful refinancing experience, consider the following tips:

Shop for lenders

Take the time to shop around and compare offers from multiple lenders. This can help you secure the best interest rate and terms for your refinancing.

Negotiate interest rates

Don’t hesitate to negotiate with lenders to try and secure a lower interest rate. Use other offers as leverage and present your creditworthiness as a strong case for a better rate.

Read the fine print

Carefully review all loan documents and disclosures before signing. Ensure that you understand the terms, conditions, and any potential fees or penalties associated with the refinancing.

Seek professional advice

Consider consulting with a financial advisor or mortgage professional to guide you through the refinancing process. Their expertise can help you make informed decisions and navigate any complexities.

Consider future plans

Take into account your long-term financial goals and plans before refinancing. Consider how the new loan terms align with your future plans and whether refinancing makes sense in the context of your overall financial strategy.

Conclusion

Refinancing a home equity loan can provide homeowners with the opportunity to save money, access cash, and improve their financial situation. By understanding the refinancing process, exploring different options, and considering the potential benefits and drawbacks, you can make an informed decision. Remember to assess your financial goals and seek professional advice when necessary. With careful planning and research, you can navigate the refinancing process and ensure a successful outcome.

How To Access Up To One Million Dollars Without Any Proof Of Income