In this article, you will explore the key distinctions between secured and unsecured loans. Whether you’re considering a loan for a new car or looking to fund a home renovation, understanding the differences between these two types of loans is essential. By the end of this article, you’ll have a clear understanding of secured and unsecured loans, helping you make an informed decision when it comes to your financial needs. So, let’s dive in and explore the nuances of these loan options!

Secured Loans

Definition

Secured loans are a type of loan that requires collateral to secure the loan. Collateral can be any valuable asset that the lender can take ownership of if you fail to repay the loan. This provides the lender with a guarantee that they will be able to recover the outstanding balance in case of default.

Collateral

Collateral is a crucial component of secured loans. It serves as a security for the lender and reduces the risk involved in lending money. Common forms of collateral include real estate, vehicles, investments, or other valuable assets that have a market value. The value of the collateral will typically determine the loan amount that you can borrow.

Loan Amount

Secured loans typically allow you to borrow a larger amount compared to unsecured loans. Since the loan is backed by collateral, lenders feel more comfortable extending higher loan amounts. The loan amount will depend on the value of the collateral and the lender’s assessment of your ability to repay the loan.

Interest Rate

Secured loans generally have lower interest rates compared to unsecured loans. Since the lender has the collateral to fall back on, the risk of default is reduced. This translates to lower interest rates for borrowers. The interest rate will vary based on factors such as the loan term, creditworthiness, and the prevailing market rates.

Credit Requirements

One significant advantage of secured loans is that they are more accessible to individuals with less-than-perfect credit. While a good credit score can positively impact the interest rate, you may still be able to secure a secured loan even with a lower credit score. Lenders are more interested in the collateral and your ability to repay the loan on time.

Risk

Secured loans carry less risk for lenders due to the presence of collateral. As a borrower, it is essential to evaluate your financial situation carefully to ensure that you can meet the repayment obligations. Failure to repay the loan may result in the lender taking ownership of the collateral, which can have serious consequences.

Examples

Common examples of secured loans are mortgages, auto loans, and home equity loans. In a mortgage, the property itself serves as collateral, while in an auto loan, the vehicle being financed acts as collateral. Home equity loans use the borrower’s home equity as collateral.

Advantages

Secured loans offer several advantages for borrowers. These include:

- Access to higher loan amounts: Due to the presence of collateral, lenders are more willing to offer larger loan amounts.

- Lower interest rates: Secured loans typically come with lower interest rates compared to unsecured loans.

- Easier qualification: Secured loans are often more accessible to individuals with lower credit scores.

- Longer repayment terms: Secured loans may offer longer repayment terms, making it easier to manage monthly payments.

Disadvantages

Despite the advantages, there are some disadvantages to consider when opting for a secured loan:

- Risk of losing collateral: If you fail to repay the loan, the lender has the right to seize and sell the collateral to recover their losses.

- Longer repayment term: While longer repayment terms can be beneficial, they also mean more interest paid over time.

- Limited options for collateral: Some borrowers may struggle to provide suitable collateral.

This image is property of www.investopedia.com.

Unsecured Loans

Definition

Unsecured loans are a type of loan that does not require collateral. Unlike secured loans, they are based solely on the borrower’s creditworthiness and ability to repay the loan.

Collateral

Unsecured loans do not require collateral. Instead, lenders rely on the borrower’s creditworthiness and income to evaluate the risk of lending. This makes unsecured loans more accessible to individuals who may not have valuable assets to use as collateral.

Loan Amount

The loan amount for unsecured loans is typically lower compared to secured loans. Since there is no collateral to secure the loan, lenders may impose stricter limits on the amount they are willing to lend. The loan amount will depend on factors such as your credit history, income, and the lender’s policies.

Interest Rate

Unsecured loans generally have higher interest rates compared to secured loans. The higher interest rate compensates for the increased risk undertaken by the lender. The interest rate will vary depending on factors such as creditworthiness, loan term, and prevailing market rates.

Credit Requirements

Creditworthiness plays a significant role in obtaining an unsecured loan. Lenders will assess your credit history, credit score, and income to determine your eligibility. A strong credit history and a high credit score will improve your chances of qualifying for an unsecured loan and securing a favorable interest rate.

Risk

Unsecured loans carry more risk for lenders as there is no collateral to fall back on if the borrower defaults. When considering an unsecured loan, borrowers should carefully evaluate their financial capacity to ensure they can meet the repayment obligations. Failing to repay the loan may result in damaging your credit history and facing legal consequences.

Examples

Examples of unsecured loans include personal loans, credit cards, and student loans. Personal loans are often used for various purposes, such as debt consolidation or covering unexpected expenses. Credit cards provide a line of credit that can be used for purchases, and student loans are designed to finance education expenses.

Advantages

While unsecured loans may have higher interest rates and stricter credit requirements, they offer several advantages:

- No collateral required: Unsecured loans do not require any collateral, making them accessible to a wider range of individuals.

- Faster approval process: Since there is no need for collateral evaluation, the approval process for unsecured loans is typically faster.

- Flexibility: Unsecured loans offer flexibility in terms of how the funds can be used, whether for debt consolidation, home improvements, or other personal needs.

- No risk of losing collateral: Unlike secured loans, there is no risk of losing valuable assets if you are unable to repay the loan.

Disadvantages

It’s important to consider the disadvantages associated with unsecured loans before making a decision:

- Higher interest rates: Due to the increased risk for lenders, unsecured loans often come with higher interest rates.

- Stricter credit requirements: Borrowers need to have a strong credit history and a steady income to qualify for unsecured loans.

- Lower loan amounts: The absence of collateral may lead to lower loan amounts compared to secured loans.

- Potential impact on credit: A default on an unsecured loan can significantly damage your credit history and make it harder to obtain credit in the future.

This image is property of www.investopedia.com.

Key Differences

Collateral Requirement

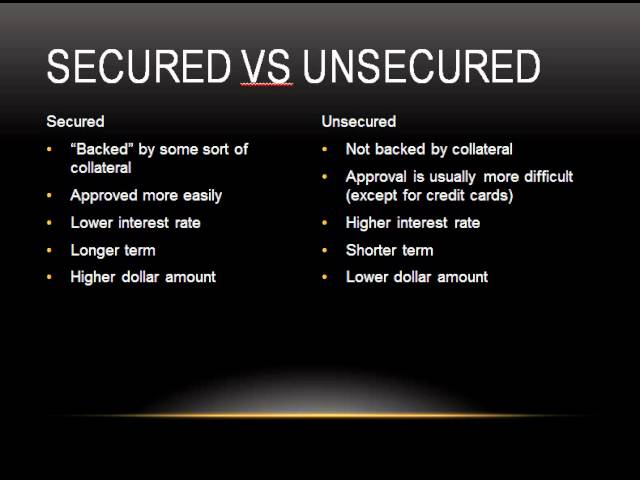

The primary difference between secured and unsecured loans lies in the collateral requirement. Secured loans require collateral, while unsecured loans do not. Collateral provides security for the lender and reduces the risk of lending.

Loan Amount

Secured loans generally allow borrowers to access larger loan amounts, primarily because the loan is backed by collateral. On the other hand, unsecured loans typically offer lower loan amounts due to the absence of collateral and the higher risk involved for lenders.

Interest Rate

Secured loans often come with lower interest rates compared to unsecured loans. Since the lender has collateral to fall back on, the risk of default is reduced. Unsecured loans, on the other hand, have higher interest rates as lenders are taking on a higher level of risk.

Credit Requirements

Secured loans are more forgiving when it comes to credit requirements. While a good credit score can still positively impact the interest rate offered, individuals with lower credit scores can still qualify for secured loans based on the collateral provided. Unsecured loans, however, place more emphasis on creditworthiness and may require a higher credit score to qualify.

Risk

Secured loans carry less risk for lenders as they have collateral to recover their losses in case of default. Unsecured loans present a higher risk for lenders as there is no collateral to fall back on, making credit history and income assessment crucial factors for approval.

Examples

As mentioned earlier, common examples of secured loans include mortgages, auto loans, and home equity loans. Examples of unsecured loans include personal loans, credit cards, and student loans.

This image is property of qph.cf2.quoracdn.net.

Factors to Consider

Purpose of Loan

The purpose of the loan should be one of the primary considerations when deciding between secured and unsecured loans. For specific purposes such as purchasing a home or a vehicle, a secured loan may be the better option due to the ability to access higher loan amounts and generally lower interest rates. For more flexible purposes or smaller expenses, an unsecured loan may be suitable.

Ability to Repay

Your ability to repay the loan is crucial to avoid default and potential financial difficulties. Consider your income stability and financial obligations before deciding on a loan type. If you are confident in your ability to make regular payments, a secured loan may offer more favorable terms. However, if you are uncertain about your financial situation or have irregular income, an unsecured loan may be a safer choice.

Credit History

Your credit history plays a significant role in the loan application process. Lenders will assess your creditworthiness to determine whether you qualify for a loan and what interest rate you will be offered. If you have a strong credit history and a high credit score, you may have more options and better terms with both secured and unsecured loans.

Risk Tolerance

Consider your risk tolerance when choosing between secured and unsecured loans. Secured loans provide more security for lenders but require collateral, which may put your valuable assets at risk. Unsecured loans carry higher interest rates and may have stricter credit requirements, but they do not require collateral. Assess your comfort level with each loan type to make an informed decision.

In conclusion, understanding the difference between secured and unsecured loans is essential when considering borrowing money. Secured loans offer the advantage of higher loan amounts, lower interest rates, and easier qualification for individuals with lower credit scores. However, the risk of losing collateral and potential impact on credit are important considerations. Unsecured loans, while having higher interest rates and stricter credit requirements, provide the benefit of no collateral requirement and faster approval process. Consider factors such as the purpose of the loan, ability to repay, credit history, and risk tolerance to make the best decision for your financial situation.

This image is property of i.ytimg.com.