Are you a student trying to navigate the world of student loans? If so, you’re not alone. Understanding how student loans work is crucial in making informed decisions about your education and future finances. In this article, we will explore the key differences between federal and private student loans, shedding light on the pros and cons of each option. By the end, you’ll have a clearer understanding of which type of loan may be the best fit for your unique situation. So, let’s dive in and demystify the world of student loans together!

Federal Student Loans

Federal student loans are loans provided by the government to help students and their families afford the cost of higher education. These loans typically have low interest rates and flexible repayment options. There are several types of federal student loans available to students, including Direct Subsidized Loans, Direct Unsubsidized Loans, and Direct PLUS Loans.

Types of Federal Student Loans

- Direct Subsidized Loans: These loans are available to undergraduate students who demonstrate financial need. Interest on subsidized loans is paid by the government while the borrower is in school, during the grace period, and in deferment.

- Direct Unsubsidized Loans: Both undergraduate and graduate students can apply for unsubsidized loans. Unlike subsidized loans, interest on unsubsidized loans accumulates while the borrower is in school.

- Direct PLUS Loans: These loans are available to graduate or professional students as well as parents of dependent undergraduate students. PLUS loans have higher interest rates and require a credit check.

Eligibility Criteria for Federal Student Loans

To be eligible for federal student loans, you must be a U.S. citizen or eligible non-citizen and have a valid Social Security number. You must also be enrolled or accepted for enrollment in an eligible degree or certificate program at an accredited institution. Additionally, you must maintain satisfactory academic progress to continue receiving federal loan assistance.

Application Process for Federal Student Loans

To apply for federal student loans, you need to complete the Free Application for Federal Student Aid (FAFSA). The FAFSA is available online and must be submitted each year to determine your eligibility for federal aid. The application requires you to provide information about your family’s finances, including income and tax returns.

Interest Rates and Repayment Options for Federal Student Loans

Federal student loans offer fixed interest rates, meaning your interest rate will not change throughout the life of the loan. The interest rate may vary depending on the type of loan and the academic year in which it is disbursed. Federal loans also offer various repayment options, such as Standard Repayment, Graduated Repayment, Extended Repayment, and Income-Driven Repayment plans.

Benefits of Federal Student Loans

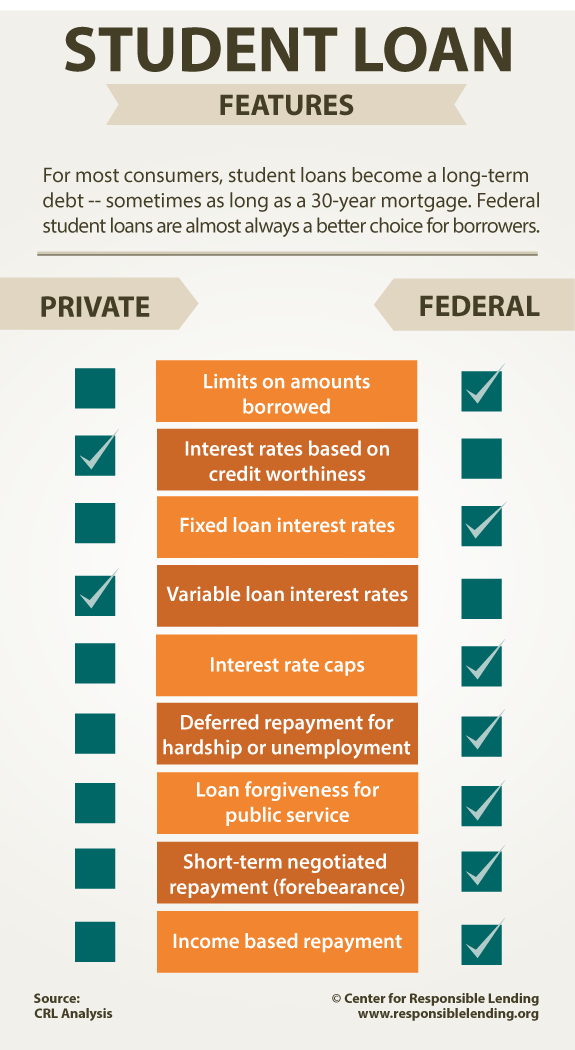

Federal student loans offer several benefits that make them an attractive option for students. Firstly, they generally have lower interest rates compared to private loans. Additionally, federal loans offer flexible repayment options to ensure that borrowers can manage their loan payments based on their income. Federal loans also provide opportunities for loan forgiveness and discharge under certain circumstances, such as working in a qualifying public service job or experiencing financial hardship.

Limitations of Federal Student Loans

While federal student loans have many advantages, there are some limitations to consider. The amount of federal loans you can borrow is limited each year, and there are lifetime limits as well. This may require you to seek alternative funding sources or consider private student loans to cover the remaining costs. Federal loans also come with certain eligibility criteria, so not all students may qualify. Additionally, federal loans have certain repayment terms and conditions that may not suit everyone’s financial situation.

Private Student Loans

Private student loans, as the name suggests, are loans provided by private lenders such as banks, credit unions, and online lenders. These loans are not backed by the government and have different terms and conditions compared to federal loans.

Types of Private Student Loans

Private student loans come in various forms, including undergraduate loans, graduate loans, and parent loans. These loans may have fixed or variable interest rates, and eligibility requirements and loan terms vary between lenders.

Eligibility Criteria for Private Student Loans

To qualify for private student loans, you generally need to have a good credit history and a steady source of income, or a creditworthy cosigner. Private lenders assess your creditworthiness to determine your ability to repay the loan.

Application Process for Private Student Loans

The application process for private student loans varies depending on the lender. You will need to submit an application, provide documentation such as proof of income and credit history, and may be required to undergo a credit check. It is advisable to compare rates and terms from multiple lenders before finalizing a loan.

Interest Rates and Repayment Options for Private Student Loans

Private student loans may offer fixed or variable interest rates, depending on the lender and the loan agreement. Variable interest rates may fluctuate over time, so it is important to consider the potential impact on your monthly payments. Private loans typically offer fewer repayment options compared to federal loans, but some lenders may offer forbearance or deferment options for borrowers facing financial hardship.

Benefits of Private Student Loans

Private student loans can provide additional financial support when federal student loans and other sources of aid do not cover the full cost of education. Private loans may have higher borrowing limits, allowing you to finance your education entirely. Additionally, private loans may offer competitive interest rates for borrowers with good credit, potentially resulting in lower total repayment amounts.

Limitations of Private Student Loans

One major limitation of private student loans is the lack of borrower protections and benefits available with federal loans. Private loans generally do not offer loan forgiveness or discharge options. Additionally, the interest rates on private loans can be higher than those on federal loans, especially for borrowers with limited credit history or poor credit scores. Private loans may also require immediate repayment or higher monthly payments, which can be challenging for recent graduates entering the job market.

This image is property of www.investopedia.com.

Choosing Between Federal and Private Student Loans

When it comes to choosing between federal and private student loans, you need to carefully consider several factors that can impact your financial well-being in the long run.

Considerations When Choosing Between Federal and Private Student Loans

- Interest Rates: Federal student loans generally have lower fixed interest rates compared to private loans, which may have variable interest rates. Consider how the interest rates will affect your monthly payments and the total cost of the loan over its lifetime.

- Repayment Options: Federal loans offer more flexibility in repayment options, such as income-driven plans and loan forgiveness programs. Private loans may have fewer repayment options, which may limit your ability to adjust payments based on your income.

- Borrowing Limits: Federal loans have annual and lifetime borrowing limits, while private loans may provide higher loan amounts. Evaluate your financial needs and the cost of your education to determine if federal loans alone will be sufficient or if you need to supplement with private loans.

Factors to Evaluate Before Choosing Between Federal and Private Student Loans

- Creditworthiness: Federal loans do not require a credit check, making them accessible to all eligible students. On the other hand, private loans consider your credit history and income, which can impact the interest rate and loan terms offered. Evaluate your creditworthiness and explore options to improve your credit if needed.

- Financial Situation: Analyze your current financial situation and future income prospects. Consider how student loan payments will fit into your budget after graduation. If you anticipate difficulty in repaying your loans, federal loans generally offer more flexible repayment options and potential for loan forgiveness.

- Long-Term Goals: Consider your long-term career goals and the potential impact of your student loan debt. Certain professions, such as public service or teaching, may qualify for federal loan forgiveness programs. Private loans may not offer similar options. Evaluate the potential benefits and limitations in relation to your chosen career path.

Ensuring you have a clear understanding of the differences between federal and private student loans and considering these factors will help you make an informed decision that aligns with your financial goals.

Repaying Student Loans

Repaying student loans is a crucial responsibility that should be carefully managed to avoid financial stress. Both federal and private student loans offer various repayment options to accommodate borrowers’ financial situations.

Repayment Options for Federal Student Loans

Federal student loans provide several repayment plans to choose from:

- Standard Repayment: This plan involves fixed monthly payments over a period of 10 years.

- Graduated Repayment: With this plan, payments start low and gradually increase every two years over a 10-year period. This option may suit borrowers with lower initial income that is expected to rise over time.

- Extended Repayment: This plan allows you to extend the repayment period up to 25 years, resulting in lower monthly payments. However, this may also increase the total interest paid over the life of the loan.

- Income-Driven Repayment (IDR) Plans: IDR plans calculate your monthly payments based on your income and family size. Plans include Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). These plans cap your monthly payments at a percentage of your discretionary income.

- Public Service Loan Forgiveness (PSLF): Borrowers working in qualifying public service jobs may be eligible for loan forgiveness after making 120 qualifying payments under an IDR plan.

Repayment Options for Private Student Loans

Private student loans have fewer repayment options compared to federal loans. However, some lenders may offer deferment or forbearance options for borrowers facing financial hardship. It is important to contact your lender to discuss available repayment plans.

Defaulting on Student Loans

Defaulting on student loans occurs when a borrower fails to make payments as required by the loan agreement. Defaulting can have severe consequences, such as damage to credit scores, collection fees, and wage garnishment. It is important to communicate with your loan servicer if you encounter difficulties in repaying your loans to explore options for deferment, forbearance, or loan modification.

This image is property of letsgotocollegeca.org.

Financial Aid and Scholarships

Before considering student loans, it is essential to explore alternative sources of funding to minimize reliance on debt.

Alternative Funding Sources Before Considering Student Loans

- Grants: Grants, such as the Federal Pell Grant, are typically awarded based on financial need and do not need to be repaid. Research and apply for grants that align with your educational goals.

- Work-Study Programs: Many colleges offer work-study programs that allow students to work part-time jobs on or off-campus to earn money for educational expenses.

- Scholarships: Scholarships are another form of aid that can significantly reduce the burden of educational costs. Research and apply for scholarships offered by schools, organizations, and private foundations. Many scholarships have specific eligibility criteria, so be sure to review them carefully before applying.

- Personal Savings: Utilize your personal savings or funds from a 529 college savings plan to cover some of the educational expenses.

Applying for Financial Aid

To access federal financial aid, including grants and student loans, you must complete the Free Application for Federal Student Aid (FAFSA). The FAFSA is available online and requires you to provide information about your family’s finances. Be sure to submit the FAFSA by the specified deadline to maximize your eligibility for aid.

Exploring Scholarships and Grants

In addition to federal aid, explore and apply for scholarships and grants offered by colleges, private organizations, and community foundations. There are scholarships available for various academic achievements, extracurricular involvement, community service, and specific fields of study. Researching and applying for scholarships can significantly reduce your reliance on student loans.

Loan Forgiveness and Discharge

Under certain circumstances, borrowers may be eligible for loan forgiveness or discharge, which can provide relief from the burden of student loan debt.

Possibilities for Loan Forgiveness with Federal Loans

- Public Service Loan Forgiveness (PSLF): Borrowers who work full-time for a qualifying employer, such as a government or non-profit organization, and make 120 qualifying payments under an IDR plan may be eligible for loan forgiveness through PSLF.

- Teacher Loan Forgiveness: Teachers who serve in low-income schools or educational service agencies for five consecutive years may be eligible for up to $17,500 in loan forgiveness.

- Loan Forgiveness for Income-Driven Repayment (IDR): Borrowers on IDR plans may be eligible for loan forgiveness after making payments for a specified period (typically 20-25 years), depending on the plan.

Options for Loan Discharge with Federal Loans

Loan discharge may be possible in certain circumstances:

- Total and Permanent Disability Discharge: Borrowers who are totally and permanently disabled may qualify for loan discharge.

- Closed School Discharge: If your school closes while you are enrolled or shortly after, you may be eligible for loan discharge.

- Borrower Defense to Repayment Discharge: If your school engaged in fraudulent or deceptive practices, you may be eligible for loan discharge.

Private Loans and Loan Discharge

Unlike federal loans, private loans generally do not offer loan forgiveness or discharge options. However, it is important to review the terms and conditions of your private loan agreement, as some lenders may offer limited discharge options in specific circumstances.

This image is property of www.responsiblelending.org.

Consolidation and Refinancing

Consolidation and refinancing can help borrowers manage their student loan debt more effectively by combining multiple loans or obtaining better repayment terms.

Consolidating Federal Student Loans

Consolidation allows you to combine multiple federal loans into a single loan, resulting in a single monthly payment. This can simplify repayment and potentially extend the repayment term. However, consolidation may not always be the best option, as it can result in a higher overall interest cost.

Refinancing Private Student Loans

Refinancing private student loans involves taking out a new loan from a private lender to pay off existing loans. This can potentially lower your interest rate, reduce monthly payments, or change your repayment terms. However, refinancing may result in the loss of certain borrower benefits and protections offered by federal loans. It is important to carefully evaluate the terms and conditions offered by different lenders before refinancing.

Resources and Assistance

Understanding the resources available and seeking assistance when needed can be beneficial in managing your student loans effectively.

Understanding Loan Servicers

Loan servicers are the companies responsible for managing and collecting loan payments on behalf of the lender. It is important to understand who your loan servicer is and how to contact them for any questions or concerns regarding your student loans. They can provide information about repayment options, deferment, forbearance, and other loan-related inquiries.

Seeking Help and Assistance

If you are facing difficulties in managing your student loans or have concerns about loan repayment, several resources are available to provide guidance and assistance. Reach out to your loan servicer, financial aid office, or student loan counselor for advice on navigating your repayment options. Additionally, many free online resources provide information and tools to help borrowers understand their rights and responsibilities when it comes to student loans.

This image is property of scholly-www.s3.amazonaws.com.

Future Trends and Considerations

The landscape of student loans and repayment options is continually evolving. Understanding potential changes and their impact on borrowers is essential for making informed decisions.

Potential Changes to Federal Student Loan Programs

Federal student loan programs may undergo changes in interest rates, repayment options, and loan forgiveness eligibility. Stay updated with any legislative or policy changes that may affect your existing or future federal loans.

Effects of Student Loan Debt on the Economy

The increasing burden of student loan debt has impacts beyond individual borrowers. High levels of student loan debt can affect economic growth as borrowers have limited ability to save, invest, or make major purchases. Monitor discussions and research related to the impact of student loan debt on the overall economy to gain insight into the broader implications of your student loan choices.

By understanding the various aspects of federal and private student loans, repayment options, loan forgiveness opportunities, and alternative funding sources, you can make informed decisions regarding your education financing. Consider your financial situation, long-term goals, and available resources to ensure you manage your student loans responsibly and minimize the financial burden in the future.